There is a quiet but powerful factor that influences how much you pay for health insurance, and most people do not fully understand it until they experience it firsthand. It is not your age, not your medical history, and not even your lifestyle in isolation. It is your location. The city you live in, or more specifically the city where your policy is issued and used, plays a decisive role in determining your premium. This concept, often described as health insurance premium by city, reflects a deeper economic reality that goes far beyond insurance companies trying to charge more. It is rooted in how healthcare costs vary across regions, how insurers manage risk, and how financial systems adapt to local cost structures. When you move from one city to another, especially from a smaller town to a large metro, you are not just changing your address. You are entering a completely different cost ecosystem, and your insurance premium adjusts accordingly.

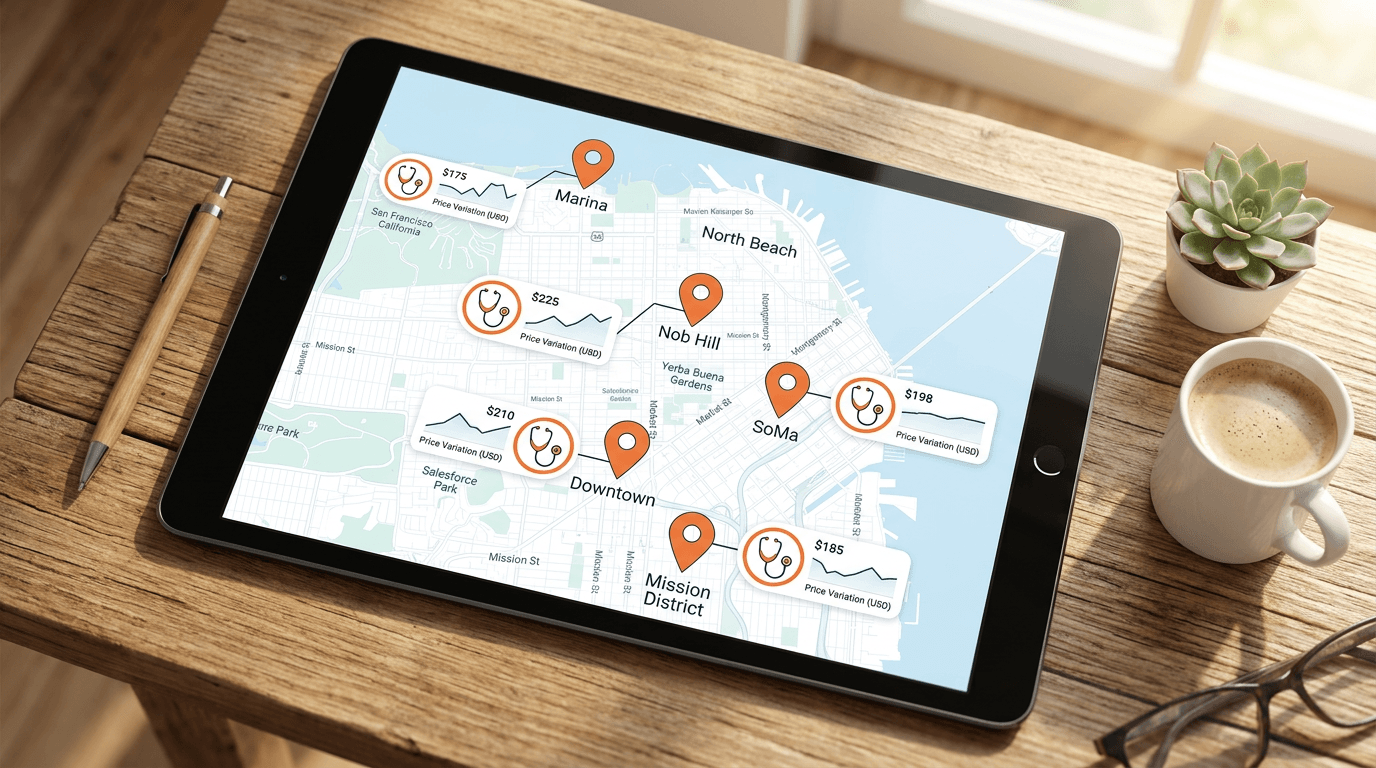

To understand why this happens, it is important to step back and look at the structure of healthcare costs in a country like India. Healthcare is not uniformly priced across cities. The cost of a hospital room, the consultation fee of a specialist, the price of surgical procedures, and even diagnostic tests vary significantly depending on where you are. In major metropolitan cities like Delhi or Mumbai, hospitals operate with higher infrastructure costs, higher salaries for medical professionals, and often more advanced equipment. These costs are passed on to patients in the form of higher bills. In contrast, cities like Lucknow or Indore typically have lower operating costs, which results in more affordable treatment. Insurance companies closely track these differences because their primary objective is to predict and manage the cost of claims. If claims are expected to be higher in a particular city, premiums must be adjusted to reflect that risk.

Why Insurers Divide Cities into Pricing Zones

Insurance companies do not price policies randomly. They use a structured system of zoning, where cities are grouped into categories based on healthcare cost levels and historical claim data. Metro cities are usually placed in the highest cost zones, while smaller towns fall into lower cost categories. This zoning system allows insurers to align premiums with expected claim expenses. For example, if the average cost of a surgery in Delhi is significantly higher than in Lucknow, the premium for a policy issued in Delhi must account for that difference. This is not just about current costs but also about future risk. Insurers analyse years of claims data to identify patterns and trends, which then inform their pricing models.

The concept of health insurance premium by city becomes particularly important when individuals relocate. A person who buys a policy in a lower cost zone may enjoy relatively low premiums initially. However, if they move to a higher cost zone and seek treatment there, the insurer may impose additional conditions such as co payment. This means that the policyholder has to bear a portion of the medical expenses out of pocket. In some cases, insurers may also require a premium revision if the policyholder officially changes their residence to a higher cost zone. These adjustments are not arbitrary. They are designed to maintain the financial balance of the insurance pool, ensuring that premiums collected are sufficient to cover claims paid.

The Hidden Financial Impact of Moving Cities

Relocating to a new city is often seen as a step forward, whether for career growth, better education, or improved lifestyle. However, the financial implications of such a move extend beyond rent, transportation, and daily expenses. Health insurance is one of the most overlooked components in this transition. When you move from a lower cost city to a metro, your exposure to higher healthcare costs increases immediately. Even if you remain healthy, your insurance policy is now tied to a cost environment that is fundamentally different from where it was originally priced. This shift in expenses is similar to how relocation impacts housing decisions, where tools that help you estimate house construction cost become essential for financial planning in a new city.

Consider a realistic scenario. A young professional purchases a health insurance policy while living in Lucknow, benefiting from lower premiums due to the city’s classification as a lower cost zone. A few years later, they move to Delhi for a better job opportunity. Their salary increases, but so does their cost of living. If they need medical treatment in Delhi, the cost of hospitalization could be significantly higher than what their policy was originally priced for. If the policy does not fully cover these higher costs, the individual may have to pay the difference out of pocket. Alternatively, if they update their policy to reflect their new location, their premium may increase substantially. In both cases, the financial impact is real and often unexpected.

Co Payment and Other Conditions That Come Into Play

One of the most common mechanisms insurers use to manage location based cost differences is co payment. This means that the policyholder agrees to pay a certain percentage of the claim amount, while the insurer covers the rest. Co payment clauses are often triggered when treatment is taken in a higher cost zone than the one for which the policy was originally priced. For example, a policyholder from a lower cost city who undergoes treatment in a metro hospital may be required to pay a fixed percentage of the bill.

This introduces an additional layer of financial planning that many people overlook. Health insurance is often perceived as a complete safety net, but in reality, it comes with conditions that can significantly affect out of pocket expenses. Understanding these conditions is crucial for making informed decisions. It is not enough to look at the sum insured or the premium. You need to evaluate how the policy behaves under different scenarios, including relocation. This is where the concept of health insurance premium by city becomes more than just a pricing factor. It becomes a determinant of financial risk.

The Broader Economic Logic Behind Location Based Pricing

The idea that your location affects your insurance premium is not unique to India. It is a global practice rooted in fundamental economic principles. Insurance operates on the concept of risk pooling, where premiums collected from many individuals are used to pay claims for a few, reflecting the broader impact of technology on financial services as data, analytics, and digital systems increasingly influence how risks are assessed and priced. For this system to remain sustainable, premiums must reflect the expected cost of claims. Since healthcare costs vary by location, it is logical for premiums to vary as well.

This variation is also influenced by broader economic factors such as urbanization, income levels, and access to healthcare infrastructure. Metro cities tend to attract higher income populations, which drives demand for advanced medical services. This, in turn, increases the cost of healthcare. At the same time, the concentration of high quality hospitals and specialists in these cities leads to more frequent and expensive treatments. Insurance companies incorporate all these factors into their pricing models. The result is a system where location becomes a proxy for cost and risk.

What This Means for Your Financial Planning

Understanding how your location affects your health insurance premium is not just about saving money. It is about aligning your insurance strategy with your broader financial goals. If you are planning to move to a metro city, it is important to anticipate the impact on your insurance costs and adjust your budget accordingly. This may involve upgrading your policy, increasing your sum insured, or choosing a plan that offers nationwide coverage without restrictive conditions.

It is also important to consider the long term implications. Health insurance is not a one time purchase. It is a continuous commitment that evolves with your life circumstances. As your income, lifestyle, and location change, your insurance needs will change as well. Regularly reviewing your policy and understanding how factors like location influence your premium can help you avoid unpleasant surprises and ensure that you are adequately protected.

Conclusion

The relationship between your location and your health insurance premium is a powerful reminder that financial decisions do not exist in isolation. They are shaped by a complex interplay of economic factors, industry practices, and personal choices. The concept of health insurance premium by city highlights how something as simple as your address can influence the cost and effectiveness of your financial protection.

As you plan your future, whether it involves moving cities, changing jobs, or upgrading your lifestyle, it is essential to consider the hidden financial implications of these decisions. Health insurance should not be an afterthought. It should be an integral part of your financial strategy, carefully aligned with your circumstances and goals. By understanding how location based pricing works and making informed choices, you can ensure that your insurance remains a source of security rather than an unexpected burden.

FAQ Section

Health insurance premiums vary by city because healthcare costs differ across locations. Insurers adjust premiums based on expected claim expenses in each city.

If you move to a higher cost city, your premium may increase or you may face conditions like co payment when claiming insurance.

You can keep your policy, but claims in higher cost cities may involve additional charges or restrictions depending on your insurer.

Co payment is the percentage of the claim amount that you need to pay from your own pocket while the insurer covers the rest.

You can choose a policy with nationwide coverage, upgrade your plan, or review terms related to city classification before purchasing.

Buying insurance in a metro city may cost more initially, but it can provide better coverage and fewer restrictions when accessing treatment in high cost hospitals.