Your phone rings at 9 PM. An unknown number. You pick up and within seconds, someone is threatening to show up at your office, embarrass you in front of colleagues, or worse, contact your family members. If this sounds familiar, you are not alone. Loan recovery agent harassment has become one of the most common financial complaints in India, rising sharply with the boom in personal loans and digital lending apps.

The good news: Indian law is firmly on your side. The Reserve Bank of India (RBI) has issued detailed guidelines on how recovery agents must behave. Banks and NBFCs face serious penalties if their agents cross the line. You have concrete, enforceable rights — and knowing how to complain against loan recovery agents is your single most powerful tool.

This guide walks you through exactly what constitutes illegal harassment, what the RBI says agents are not allowed to do, and a clear step-by-step process to file a complaint — from your bank’s grievance cell all the way to the RBI Ombudsman and Consumer Court. By the end, you will know precisely what to do the next time a recovery agent oversteps.

What Loan Recovery Agents Are Legally NOT Allowed to Do

Before you file any complaint, you need to know what actually qualifies as illegal behaviour. Recovery agents are hired by banks, NBFCs, and digital lending apps to follow up on overdue payments. They have a job to do — but that job comes with strict legal boundaries set by the RBI.

Under the RBI Fair Practices Code and its Guidelines on Recovery Agents (2008, updated 2022), the following actions by any recovery agent are prohibited:

- Calling before 8:00 AM or after 7:00 PM — any call outside these hours is a direct RBI violation.

- Using abusive, threatening, or humiliating language — verbal abuse is grounds for an immediate complaint.

- Contacting your employer, relatives, or neighbours without prior written consent — this is a breach of your data privacy.

- Making false claims — such as telling you they are police officers or that a court case has already been filed.

- Visiting your home without prior written notice — surprise visits are illegal.

- Refusing to show authorization documents — every agent must carry a written letter from the bank authorizing them.

- Physical intimidation or assault — this is a criminal offence under the IPC, not just a banking violation.

A recovery agent showing up with multiple people at your doorstep to intimidate you, or sending threatening WhatsApp messages at midnight, is not just being aggressive — they are breaking the law. Document every such incident carefully, because this documentation will become your strongest evidence. RBI Guidelines on Engagement of Recovery Agents

RBI Guidelines at a Glance

| RBI Guideline | What It Means For You |

|---|---|

| Calling hours: 8 AM – 7 PM only | Calls outside this window are a direct RBI violation |

| Agent must identify themselves | They must state their name, bank name, and purpose |

| No abusive, threatening language | Any verbal abuse can be reported immediately |

| Cannot discuss loan with third parties | They cannot call your boss, relatives, or neighbours |

| Must give written notice before visit | Surprise home visits without notice are illegal |

| Agent must carry authorization letter | You have the right to ask for ID and written authority |

From practical observation, many borrowers face unnecessary pressure simply because they are unaware of RBI recovery rules. Keeping communication records and understanding your legal rights can help protect you from harassment and unlawful recovery practices.

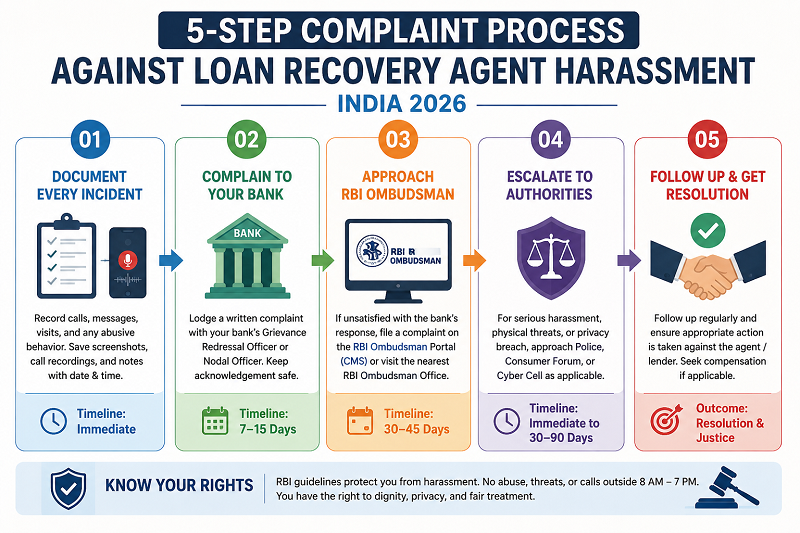

Step-by-Step: How to Complain Against Loan Recovery Agents

Filing a complaint is not complicated, but it works best when you follow the right sequence. Start at the source i.e your bank before escalating to regulators. Here is the exact process:

Step 1: Document Every Incident Immediately

Before you file anything, build your evidence file. Courts, ombudsmen, and consumer forums all rely heavily on documentation. Every time an agent contacts you inappropriately, record the following:

- Date, time, and duration of the call or visit

- Phone number or name of the agent

- Exact words used — write these down verbatim as soon as possible

- Names of any witnesses (family members, neighbours, colleagues)

- Screenshots of threatening WhatsApp messages or emails

- Call recordings — entirely legal in India when one party (you) consents

For example, consider Meera, a schoolteacher from Pune with a ₹2 lakh personal loan overdue by 45 days. A recovery agent called her school’s landline and told her principal she was a ‘fraud.’ Meera had saved the call log and a written complaint from her principal. This single piece of evidence made her grievance impossible to dismiss.

Step 2: File a Formal Complaint With Your Bank or NBFC

Every regulated bank and NBFC in India is required to have an internal grievance redressal mechanism. This is your first mandatory step before escalating to regulators.

- Visit the official website of your bank and find the ‘Grievance Redressal’ or ‘Customer Complaints’ section.

- Submit your complaint in writing — via email, registered post, or the bank’s online portal. Verbal complaints have no legal weight.

- Clearly state: your loan account number, dates of harassment, nature of the violation, and the relief you are seeking.

- Note your complaint reference number. Banks are required to acknowledge complaints within 7 days.

Banks have a mandatory 30-day window to resolve your complaint. If your complaint is not resolved satisfactorily — or is ignored — you move to Step 3.

Step 3: Escalate to the RBI Integrated Ombudsman Scheme

If the bank does not respond within 30 days, or gives you an unsatisfactory response, you can file a complaint with the RBI Integrated Ombudsman Scheme (IOS) — completely free of charge.

- Visit the official portal: cms.rbi.org.in

- Select ‘File a Complaint’ and choose the relevant bank or NBFC.

- Upload your evidence (call logs, screenshots, written records).

- The Ombudsman typically responds within 30–45 days.

- The RBI Ombudsman can award compensation of up to ₹20 lakh and direct the bank to take action against the agent.

Step 4: File a Police Complaint for Criminal Behaviour

If the recovery agent threatened physical harm, used abusive language in a public setting, or actually showed up and created a scene, file an FIR at your nearest police station. Recovery agent intimidation can fall under Section 506 (criminal intimidation) and Section 503 of the Indian Penal Code. Do not wait — a police report filed promptly strengthens every other complaint you make simultaneously.

Step 5: Approach the Consumer Forum

Under the Consumer Protection Act 2019, you can file a complaint in the District Consumer Disputes Redressal Commission. You can seek: a formal apology, compensation for mental distress, and a direction to the bank to stop the harassment. You do not need a lawyer for cases under ₹50 lakh at the district level — you can represent yourself.

Quick Reference: Where to Complain and What to Expect

| Harassment Type | Where to Complain | Timeline | Expected Outcome |

|---|---|---|---|

| Abusive language / threats | Bank's Grievance Cell | 7–15 days | Formal warning to agent |

| Calls before 8 AM or after 7 PM | RBI Ombudsman Portal | 30–45 days | Bank penalised |

| Physical intimidation / assault | Local Police Station | Immediate | FIR registered |

| Unauthorized property access | Consumer Forum + Police | 30–90 days | Legal action + compensation |

| Data privacy breach (lending app) | RBI + MeitY | 30–60 days | App delisted/fined |

| Continued harassment post complaint | RBI + Consumer Court | 60–90 days | Heavy penalty on lender |

Special Case: Harassment by Digital Loan App Recovery Agents

Digital lending app harassment deserves its own section because the tactics used are far more aggressive — and often more illegal — than those used by traditional bank agents. Complaints about apps contacting your entire phone contact list, sending WhatsApp messages to your relatives with your photo and ‘defaulter’ labels, or even morphing your images have surged since 2022.

The RBI issued a circular in September 2022 specifically restricting digital lending app practices. Under these rules, any app that operates through an NBFC or bank must follow the same recovery guidelines. Apps that operate without an RBI license are illegal to begin with.

If a digital lending app is harassing you, here is what you do in addition to the standard steps above:

- Report the app to the Google Play Store or Apple App Store as abusive — both platforms have taken down hundreds of such apps.

- File a complaint with the Ministry of Electronics and Information Technology (MeitY) at meity.gov.in if your data has been misused.

- Report to the RBI’s Sachet portal at sachet.rbi.org.in — this portal is specifically designed for complaints about unregulated entities.

- Check if the app/lender is registered: the RBI publishes a list of authorised NBFCs. If your lender is not on this list, every rupee you paid them may be recoverable.

Your Rights Even if You Have Defaulted on a Loan

This is one of the most misunderstood points in the entire debate. Many borrowers believe that because they have not paid their EMI, they somehow lose the right to be treated with dignity. That is completely false.

Defaulting on a loan does not strip you of any fundamental right. The bank has legal remedies — sending a legal notice, filing a civil suit, initiating proceedings under the SARFAESI Act — but none of those remedies include threatening you, abusing your family, or harassing you.

Consider Rahul, a self-employed professional from Mumbai whose business revenue dropped by 40% during a difficult quarter, leaving him unable to pay three EMIs on a ₹5 lakh personal loan. The recovery agent visited his home twice, abused his elderly parents, and called his wife’s office. Rahul had defaulted — but the agent’s actions were still completely illegal. Rahul filed a complaint with the RBI Ombudsman, received a formal apology from the bank in writing, and the bank waived one month’s penalty interest as part of the resolution.

Always remember: the bank’s right to recover money and your right to be treated with dignity exist simultaneously. One does not cancel the other.

How to Build a Strong Evidence File That Gets Results

A complaint without evidence is a story. A complaint with evidence is a case. Recovery agent complaints are almost always decided on the strength of documentation. Here is how to build a file that no bank or ombudsman can dismiss:

- Call logs: Your telecom provider can give you a log of all incoming calls. This proves frequency, timing, and duration.

- Call recordings: Use your phone’s built-in recorder or an app. One-party consent recording is legally valid in India.

- Written communication: Save every SMS and WhatsApp message. Screenshot with timestamps visible.

- Witness statements: A brief written note signed by anyone who witnessed the harassment adds significant credibility.

- Medical or psychological records: If the harassment caused you genuine distress, a doctor’s note can support a claim for compensation in Consumer Court.

- Your own written diary: Maintain a dated log of every incident. Even handwritten records are accepted as supporting evidence.

📌 Important: File your bank complaint via email or registered post — not a phone call. Written complaints create a timestamp and paper trail that verbal complaints simply cannot

What This Means for You — Your Next Steps

You have every right to be treated with respect, regardless of your loan status. India’s regulatory framework is actually quite strong on this issue — the RBI has the authority to penalise banks, the Consumer Court can award compensation, and the police can register criminal cases. The system works when you use it correctly.

Here is what you should do right now:

- Start your evidence file today — even if the harassment is ongoing. Document every call, message, and visit.

- Send a written complaint to your bank’s Grievance Cell within the next 7 days. Use registered email or post.

- Set a calendar reminder for 30 days. If the bank does not resolve your complaint, file immediately with the RBI Ombudsman at cms.rbi.org.in.

- If threats were physical or criminal, file a police complaint simultaneously — do not wait for the bank process.

- Consult a consumer law advocate if you want to pursue compensation through the Consumer Forum.

The most important step is the first one — do not ignore the harassment and do not pay under duress. A threatened or forced payment made under harassment may actually be legally recoverable. Assert your rights, document everything, and use the system designed to protect you.

Frequently Asked Questions

Can a loan recovery agent call me after 7 PM?

No. Under RBI Guidelines on Recovery Agents, calls are strictly permitted only between 8:00 AM and 7:00 PM. Any call outside this window is a direct violation of RBI rules. Document the call with a screenshot of your call log (showing time) and include it in your formal complaint to the bank or RBI Ombudsman.

What if a recovery agent contacts my employer or relatives?

This is prohibited. Under RBI guidelines, recovery agents cannot share your loan information with third parties — including employers, relatives, or neighbours — without your written consent. If this has happened, it is also likely a violation of the Information Technology Act and data privacy norms. File a complaint with your bank, the RBI Ombudsman, and consider reporting to MeitY if a digital lending app was involved.

Can I record a recovery agent's phone call as evidence?

Yes. In India, recording a phone call is legally permissible when one party to the conversation — which includes you as the receiver — consents to the recording. You do not need the agent’s permission. Call recordings are widely accepted as evidence in consumer forums and ombudsman proceedings. Use your phone’s built-in call recording feature or a third-party app.

What compensation can I get if my complaint is upheld?

The RBI Ombudsman can direct a bank to pay compensation for mental harassment and any financial loss caused by the agent’s actions. There is no fixed amount, but awards in the range of ₹10,000–₹1,00,000 are not uncommon for clear violations. The Consumer Court can award additional compensation — including for mental distress and legal costs — particularly if you can show that the harassment was systematic and severe.

Does filing a complaint stop the loan recovery process?

No. Filing a complaint against a recovery agent does not pause or cancel your loan repayment obligation. The bank still has the legal right to recover the outstanding amount. However, the complaint does legally compel the bank to use only lawful recovery methods going forward. Filing a complaint also puts the bank on notice, which often results in a more senior official reaching out to negotiate a repayment plan.

What if the lending app is not registered with the RBI?

If the lending app operates without an RBI-approved NBFC or bank behind it, it is an illegal lender. You can report it on the RBI Sachet portal (sachet.rbi.org.in) and to your local police station. Importantly, some legal experts argue that loans from unregistered entities are unenforceable — meaning you may have grounds to challenge the very validity of the debt. Consult a lawyer for your specific situation.

How long does the RBI Ombudsman process take?

The RBI Integrated Ombudsman Scheme has a targeted resolution time of 30–45 days for straightforward complaints. Complex cases can take up to 90 days. The process is entirely free, can be done online at cms.rbi.org.in, and does not require a lawyer. You will be asked to provide your complaint number from the bank (proving you filed internally first) and supporting documents.

Can I file a complaint if I have already paid the loan fully?

Yes. If you suffered harassment during the loan recovery process, you can still file a complaint — even after paying off the loan. The RBI Ombudsman and Consumer Courts can entertain such complaints. The compensation you seek would be for the mental distress and harassment suffered, not for any ongoing loan issue.

One Response

Good post! We will be linking to this particularly great post on our site. Keep up the great writing