Your salary gets credited on the 5th. The auto-debit for your mutual fund SIP fires on the 10th. Two thousand rupees leave your account and go — somewhere. You probably know, in a vague way, that a fund house is involved. But what exactly happens between your bank account and the stock market? Who is making decisions about your money, how are they regulated, and how do they earn from the arrangement? Understanding the asset management company sitting in the middle of every SIP transaction is not abstract finance theory. It is practical knowledge that will change how you read a fund fact sheet, evaluate an expense ratio, and choose between two funds with nearly identical return histories. By the end of this article, you will understand the legal structure, the money flow, the regulation, and the business model of an AMC in plain terms — with specific numbers that matter for an Indian investor.

The Legal Difference Between an AMC and a Mutual Fund

Most investors use the terms AMC and mutual fund interchangeably. They are not the same entity, and understanding the difference protects you from a specific mistake & confusing the performance of a fund house with the structure that safeguards your money.

A mutual fund in India is a trust. Legally, it is set up under the Indian Trusts Act of 1882. The mutual fund trust holds your money. It does not invest your money. It does not make decisions about where your money goes. The trust exists specifically so that investor assets are legally separated from the company running the show.

The asset management company is that company. An AMC is a corporate entity registered under the Companies Act, licensed by SEBI, and appointed by the trustees of the mutual fund trust to manage the pooled money. The AMC employs the fund managers, runs the research desk, handles operations, and makes the investment calls. But the AMC does not own the money it manages. Your units in a mutual fund are a claim on the trust assets — not on the AMC’s balance sheet.

This separation matters because if an AMC goes bankrupt, your investment does not go with it. The trust assets are ring-fenced. SEBI requires that a separate custodian — typically a bank or a SEBI-registered custodial entity — holds the actual securities on behalf of the trust. The AMC cannot raid the fund to pay its own creditors.

This is not theoretical protection. It is the structural reason why mutual funds in India are considered safer than parking money with a finance company or a chit fund — where the operator and the pooled money sit in the same legal container.

How the Money Actually Flows from Your SIP to the Market

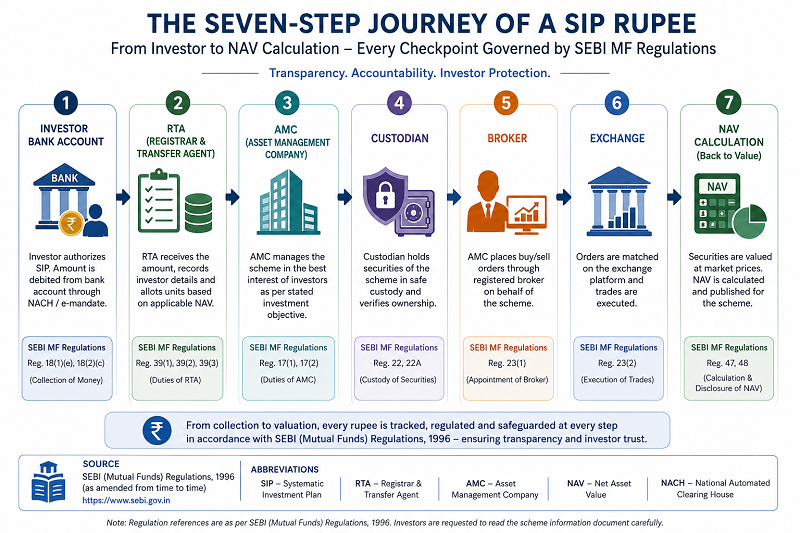

An asset management company is the operational brain of the arrangement, but the money touches several entities before a single share gets purchased. Understanding this flow helps you spot where costs enter.

When your SIP debit hits, the money goes to the AMC’s collection account via your bank or a payment aggregator. The AMC’s registrar and transfer agent companies like CAMS or KFintech updates your unit account and sends the money to the custodian. The custodian holds it in a settlement account. The fund manager places buy orders for securities through SEBI-registered brokers. The securities land in the custodian’s demat account. Your NAV is calculated every business day based on the market value of those securities minus the fund’s liabilities, divided by the number of outstanding units. The daily NAV calculation is not done casually. SEBI mandates that it be calculated and published by a specific cut-off time each day. Missing the cut-off on a given day means your purchase gets the next business day’s NAV. This is why large SIP amounts particularly in liquid funds are time-sensitive in a way that smaller retail SIPs are not.

Consider Rohan, a software engineer in Hyderabad earning ₹95,000 a month, who set up SIPs in three different funds — a large-cap fund, a mid-cap fund, and a liquid fund — from the same fund house. Even though all three are managed by the same AMC, each fund is a separate trust scheme with its own pool of securities, its own NAV, and its own risk profile. Rohan’s money in the liquid fund cannot be used to shore up a bad position in the mid-cap fund. This separation is enforced by the custodian structure and audited by SEBI.

What a Fund Manager Actually Does Inside an AMC

The fund manager is the face of the AMC, but the role is more constrained than most investors realise. This constraint is actually good news for you.

Every mutual fund scheme operates under a Scheme Information Document and a Statement of Additional Information. These documents are filed with and approved by SEBI to define the investment mandate. A large-cap fund’s mandate requires it to invest a minimum of 80 percent of its corpus in the top 100 companies by market capitalisation. The fund manager cannot decide one morning to shift the entire corpus into small-cap stocks because they personally believe small-caps will outperform. The mandate is a legal constraint, not a guideline.

Within the mandate, the fund manager leads a research team that analyses companies, sectors, valuations, and macro signals. Buy and sell decisions are typically reviewed by an investment committee, not left to one person. Most large AMCs have a chief investment officer sitting above the fund managers with oversight authority.

Asset management company is the entity that employs this entire team, pays their salaries, funds the research infrastructure, and importantly earns money from the fund’s investors through a mechanism called the total expense ratio.

I have personally noticed whenever a well-known fund manager exits an AMC, investor sentiment tends to shift quickly. Based on reader interactions and market behaviour, many investors either pause fresh SIPs or reassess their holdings until the AMC demonstrates continuity in strategy and performance.

How an AMC Earns Money — and What It Costs You

This is the section most fund marketing does not want to explain clearly. The AMC earns a fee called the total expense ratio, or TER. It is expressed as an annual percentage of the fund’s assets under management, and it is deducted daily from the NAV before the number is published. You never see a direct deduction from your account — but it is being taken every single day.

SEBI caps the TER an AMC can charge based on the size of the fund. Larger funds charge lower TER because SEBI applies a slab structure — as AUM grows, the maximum allowed TER falls. This benefits investors in large, popular funds and is one reason AUM size matters when comparing two otherwise similar schemes.

| Fund Category | Approximate TER Range | Direct Plan Saving vs Regular | Lock-in Period |

|---|---|---|---|

| Active Equity Fund | 0.5% to 2.25% per year | 0.5% to 1.0% lower in Direct Plans | None |

| Debt Fund | 0.25% to 1.50% per year | 0.2% to 0.6% lower in Direct Plans | None |

| Index Fund | 0.05% to 0.50% per year | Usually minimal difference | None |

| ELSS Fund | 0.5% to 2.25% per year | 0.5% to 1.0% lower in Direct Plans | 3 Years |

| Liquid Fund | 0.10% to 0.50% per year | Usually minimal difference | None |

When you invest in a regular mutual fund plan, you usually buy it through someone else’s app, website, or service. That company helping you buy the fund earns money for bringing you as a customer. To cover this cost, the mutual fund adds a small extra charge to your investment every year.

When you buy a direct plan through the AMC’s own website or through an RTA portal, there is no distributor in the chain, so the TER is lower and your NAV is slightly higher every single day.

At WealthBuilding when we model the long-term impact of the direct vs regular plan difference for a investor in their 30s running a SIP of 10,000 rupees a month over 20 years, the compounded difference consistently comes out to several lakhs. The headline return numbers on a fund comparison website almost never adjust for this because they pull scheme-level data without specifying which plan. Always check whether a return you are seeing applies to the direct or regular plan.

What SEBI Actually Regulates in an AMC

Investors often assume SEBI regulation means SEBI endorsement that a SEBI-registered AMC has been vetted for returns or safety. It means neither. What SEBI regulation does cover is specific and genuinely protective.

- SEBI mandates that AMC promoters maintain a minimum net worth.

- SEBI requires disclosure of the full portfolio of every scheme, every month, within 10 days of month end. SEBI regulates how risk is categorised & communicated & the Risk meter on every fund fact sheet is a SEBI-mandated disclosure, not a voluntary marketing choice.

- SEBI also regulates cross-dealing, meaning an AMC cannot buy securities from its own group companies at inflated prices to benefit the parent at the expense of fund investors.

- SEBI requires that any change in fundamental attributes of a scheme — its mandate, its benchmark, or its fee structure — triggers an exit window for investors who disagree with the change.

Consider Priya, a homemaker in Jaipur managing the household’s savings, who invested in a balanced advantage fund five years ago through her bank’s relationship manager. When the fund house later revised its rebalancing model — a fundamental attribute change — SEBI required the AMC to notify all unitholders and give them a 30-day window to exit without an exit load. Priya’s bank, unfortunately, never explained this to her. She did not exit and did not realise the mandate had changed. This is the gap between SEBI regulation existing on paper and investors actually benefiting from it — it requires investors to read fund communications, not just SIP statements.

What an AMC Does With Your Money When Markets Are Falling

This is the question most financial content avoids because the answer is uncomfortable. When equity markets fall 20%, an AMC managing an equity fund does not switch to cash to protect your returns. It cannot. The mandate requires it to stay invested in equities within the parameters of the SID. A pure equity fund cannot legally park 80 percent of the corpus in fixed deposits because the fund manager is nervous about valuations.

This is not negligence. It is the structure you signed up for. The fund mandate defines the risk the fund is permitted to take. You chose that fund. The AMC’s job is to stay within mandate, make the best investment decisions possible within that constraint, and communicate clearly about what is happening.

Where AMCs do have discretion in falling markets is in relative positioning by moving from higher-risk stocks within the equity universe to more stable ones, raising cash up to the permitted limit, or reducing cyclical exposure. Index funds and ETFs have even less discretion & they must track the index mechanically regardless of market conditions.

The lesson for an Indian household managing a portfolio through an AMC is straightforward. The AMC is a professional manager operating within SEBI-defined rules. It is not a safety net, not a guaranteed return generator, and not an entity that owes you a specific outcome. It owes you professional management, regulatory compliance, and transparent disclosure. Returns are the outcome of markets, mandates, and skill — in roughly that order of importance.

What You Now Understand That Most SIP Investors Do Not

Most Indian investors treat a mutual fund as a product and an AMC as its manufacturer. The more accurate picture is that an AMC is a regulated service provider managing a pool of assets held in a legal trust on your behalf, under a mandate you agreed to when you bought the fund, under SEBI oversight that protects your structural rights even when it cannot protect your returns.

The most common mistake Indian inventors make in this context is selecting a fund based entirely on the three-year return number without reading the mandate, checking the expense ratio, or distinguishing between the direct and regular plan — all three of which sit inside the AMC structure and directly affect what you actually earn.

Before your next SIP review, take these specific steps:

- Check whether your existing SIPs are in the direct plan or the regular plan, and note the TER difference on AMFI’s publicly available expense ratio disclosure page

- Read the one-page scheme summary of your top two funds and confirm the investment mandate matches the category you believe you are invested in

- Check whether your fund manager has changed in the past 12 months — the AMC must disclose this in the monthly fact sheet

- If you are in ELSS for tax saving under Section 80C, confirm whether you are in the direct plan and whether the three-year lock-in applies per SIP instalment rather than to the total investment date

An asset management company is not a mysterious institution. It is a licensed, regulated, disclosed entity operating in your portfolio right now. Reading its disclosures takes 20 minutes and will teach you more than any financial influencer video will in an hour.

Frequently Asked Questions

What is the difference between an AMC and a mutual fund in simple terms?

A mutual fund is a legal trust that holds investor money in a ring-fenced structure. An asset management company is the regulated firm appointed by the trustees to manage that money — making investment decisions, running operations, and earning a fee called the expense ratio. Your money sits in the trust, not on the AMC’s balance sheet, which means AMC financial trouble does not directly endanger your investment. Always check that both the trust scheme and the AMC are SEBI-registered before investing.

How does an AMC make money from my SIP?

The AMC deducts its fee every day from the fund’s NAV as a fraction of the total expense ratio. You never see a line-item deduction — the NAV you see every evening is already net of that day’s fee slice. The annual TER on an active equity fund can be between 0.5 and 1.75 percent, which on a 10 lakh corpus means between 5,000 and 17,500 rupees per year going to the fund house, regardless of whether the fund made money for you that year.

Can an AMC use my money for something other than what is written in the fund mandate?

No. SEBI requires each scheme to operate strictly within the mandate defined in its Scheme Information Document. A large-cap fund must keep at least 80 percent in the top 100 companies by market cap. Any deviation is a regulatory violation subject to SEBI action. This is one reason the SID is worth reading before investing — it is a legal document that constrains what the AMC can do with your money.

What happens to my mutual fund money if the AMC shuts down?

Your units are a claim on trust assets, not on the AMC. If an AMC loses its licence or shuts down, SEBI steps in to arrange for a transfer of the scheme to another AMC, or an orderly redemption of units at fair NAV. The custodian holding the securities is an independent entity, so the AMC’s creditors cannot access those securities. This is a structural protection specific to the Indian mutual fund regulatory framework.

What is SEBI's role in regulating AMCs in India?

SEBI registers and regulates all AMCs operating in India under the SEBI (Mutual Fund) Regulations 1996. It sets limits on expense ratios, mandates monthly portfolio disclosure, enforces investment mandate compliance, caps concentration in any single stock or sector, and investigates investor complaints. SEBI does not guarantee returns and does not vet which AMCs produce better performance — it regulates conduct and structure, not outcomes.

Is the expense ratio in mutual funds tax deductible?

No. The TER is not separately deductible from your taxable income. It is already factored into the NAV before your gains are calculated. When you redeem units, your capital gain is based on the difference between your purchase NAV and your redemption NAV — both of which are already net of all TER deductions during the holding period. Equity mutual fund gains above 1.25 lakh rupees per year are taxed at 12.5 percent as long-term capital gains if held over one year.

How do I check whether my AMC is following SEBI rules

SEBI publishes enforcement actions and orders on its website at sebi.gov.in. Every AMC must publish a monthly fact sheet with the current portfolio, expense ratio, and fund manager details on its own website and on AMFI’s website at amfiindia.com. If you want to check whether a specific fund’s TER has changed, AMFI publishes a scheme-wise TER disclosure that is updated regularly.

Does the AMC have any obligation if my fund performs badly?

The AMC has a fiduciary obligation to manage the fund in the best interests of unitholders, within the mandate. It has no obligation to produce positive returns or to match inflation. Underperformance relative to benchmark is not a regulatory violation — it is a reason for you to evaluate whether to continue holding the fund. Where the AMC does have regulatory obligations is in disclosure, mandate compliance, and conflict-of-interest management. SEBI receives investor complaints about AMC conduct, not about return outcomes.