Introduction

Flipkart Pay Later interest rate is 24% per annum when you convert purchases to EMI, plus a 1.5% processing fee on the loan amount. However, if you pay your entire bill by the 5th of the following month, you pay zero interest — making it a genuinely interest-free credit option for short-term use.

This article breaks down every charge, shows you real EMI calculations, and tells you exactly when Flipkart Pay Later costs you money vs. when it’s free.

Flipkart Pay Later: All Charges at a Glance (2026)

| Charge Type | Amount |

|---|---|

| Interest rate (EMI option) | 24% per annum |

| Processing fee (EMI) | 1.5% of loan amount |

| Interest if paid in full by due date | ₹0 (zero) |

| Monthly usage fee | Based on credit limit (see below) |

| Late payment fee | ₹100 to ₹600 + GST |

| No Cost EMI products | Processing fee only (~₹100–200) |

Option 1: Pay in Full Next Month — Zero Interest

If you buy something today and pay the complete outstanding amount by the 5th of the next month, Flipkart Pay Later charges you nothing extra. No interest, no processing fee.

This is essentially a free 30-day credit window — better than many credit cards.

Best for: Purchases you can comfortably repay within a month.

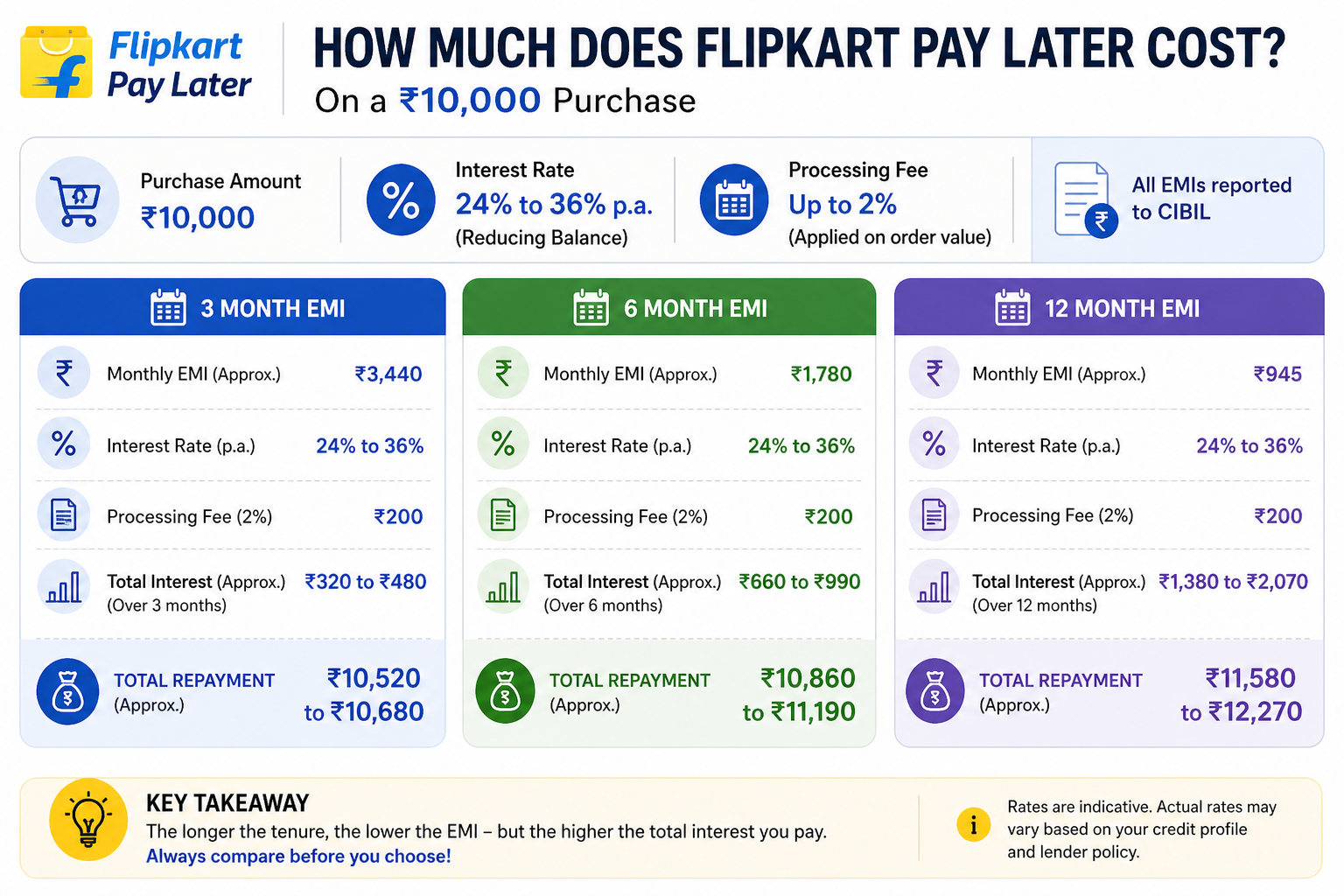

Option 2: Pay Later EMI — 24% Interest + 1.5% Processing Fee

If you convert your purchase to monthly EMIs, Flipkart charges:

- 24% p.a. interest (calculated on reducing balance)

- 1.5% processing fee upfront on the loan amount

Real EMI Calculation Example

Say you buy a ₹10,000 product and convert it to a 6-month EMI:

| Component | Amount |

|---|---|

| Loan amount | ₹10,000 |

| Processing fee (1.5%) | ₹150 |

| Interest (24% p.a. × 6 months) | ₹1,200 |

| Total payable | ₹11,350 |

| Monthly EMI (approx.) | ₹1,891 |

Compare this to a credit card at 12–16% — Flipkart Pay Later EMI is significantly more expensive for the same purchase. Use it only if you have no other option.

Monthly Usage Fee (New Charge — Important to Know)

Flipkart now charges a monthly fee based on your Pay Later credit limit, regardless of whether you’ve converted to EMI or not. This applies just for having the limit active and using it.

- Fee is charged monthly, not per transaction

- GST applies on the fee amount (rate depends on your state)

- If you don’t use your Pay Later limit in a month, no fee is charged

Tip: If you’re not actively using Pay Later, keeping zero usage that month avoids the fee entirely.

No Cost EMI: What It Means and What You Actually Pay

On select products, Flipkart offers No Cost EMI through Pay Later. Here’s the truth about it:

- The interest is subsidized by the seller or Flipkart — you don’t pay 24%

- You typically pay only a processing fee of around ₹100–200

- This is genuinely the cheapest way to use Pay Later EMI

How to spot it: Look for “No Cost EMI” tag on the product page. Not all products qualify.

Flipkart Pay Later vs Credit Card: Which Costs More?

| Feature | Flipkart Pay Later EMI | Credit Card EMI |

|---|---|---|

| Interest rate | 24% p.a. | 12–36% p.a. (varies by card) |

| Processing fee | 1.5% | ₹199–500 flat (most cards) |

| Interest-free period | Up to ~30 days | 45–55 days |

| Credit limit | Up to ₹1 lakh | Depends on card |

| Impact on credit score | Yes (via NBFC partner) | Yes |

Verdict

For EMI purchases, a credit card with 12–18% interest is usually cheaper. Use Flipkart Pay Later EMI only if you don’t have a credit card or are buying a No Cost EMI product.

Flipkart Pay Later Eligibility (2026)

Not everyone gets access automatically. Flipkart (through NBFC partners like IDFC FIRST Bank, Kotak Mahindra Bank, and Axis Bank) evaluates:

- Age: 18 years or above

- Documents: Valid PAN + Aadhaar linked to mobile number

- Credit score: ~750 or higher preferred

- Flipkart history: Active account with good purchase/payment history

- KYC: Completed verification required

Even if you meet all criteria, the final approval and credit limit is decided by Flipkart’s banking partners — not Flipkart itself.

Late Payment Charges: What Happens If You Miss the Due Date

Missing your Pay Later due date (5th of every month) results in:

- Late fee: ₹100 to ₹600 depending on outstanding amount, plus GST

- Negative CIBIL impact: Late payments are reported to credit bureaus

- Possible suspension of your Pay Later facility

Best practice: Enable AutoPay in your Flipkart account to avoid this entirely.

How to Activate Flipkart Pay Later

- Open Flipkart App → Go to My Account

- Tap Pay Later → Click Activate

- Complete KYC: Enter PAN + Aadhaar details

- Verify via OTP

- Wait for approval (usually instant to 24 hours)

- At checkout, select Pay Later as your payment method

How to Pay Your Flipkart Pay Later Bill

- Open Flipkart App → My Account → Pay Later

- Tap Pay Bill or Pay EMI

- Choose payment method: UPI, Net Banking, or Debit Card

- Pay before the 5th of every month to avoid interest and late fees

Key Tips to Use Flipkart Pay Later Wisely

- Pay in full by the 5th — this is the only way to use it completely free

- Avoid EMI for regular purchases — 24% is expensive; use a credit card instead

- Only use EMI for No Cost EMI products — where interest is already waived

- Keep your usage below 30% of limit — helps maintain/improve credit score

- Never miss the due date — late fees and CIBIL impact are not worth it

Frequently Asked Questions

What is the Flipkart Pay Later interest rate?

The interest rate is 24% per annum for EMI purchases. If you pay your full bill by the 5th of the following month, the interest rate is effectively 0% — no interest charged.

Is Flipkart Pay Later interest-free?

Yes, but only if you pay the complete outstanding amount by the 5th of the next month. Convert to EMI and you’ll pay 24% p.a. + 1.5% processing fee.

What is the processing fee on Flipkart Pay Later EMI?

1.5% of the loan amount is charged as a processing fee when you opt for EMI. For a ₹10,000 purchase, that’s ₹150.

What is the late payment fee on Flipkart Pay Later?

Late fees range from ₹100 to ₹600 plus GST, depending on your outstanding amount. Missing the due date also negatively affects your CIBIL score.

Who provides Flipkart Pay Later?

Flipkart partners with RBI-regulated NBFCs and banks including IDFC FIRST Bank, Kotak Mahindra Bank, and Axis Bank to offer the Pay Later facility.

What is the credit limit on Flipkart Pay Later?

The credit limit can go up to ₹1 lakh. Your actual limit depends on your Flipkart purchase history, credit score, and KYC verification.

Does Flipkart Pay Later affect CIBIL score?

Yes. Since it’s offered through regulated financial institutions, your usage and repayment behavior are reported to credit bureaus. Late or missed payments will lower your CIBIL score.

What is Flipkart Pay Later No Cost EMI?

On select products, Flipkart waives the 24% interest and you pay only a small processing fee (typically ₹100–200). The interest is subsidized by the seller or Flipkart. Look for the “No Cost EMI” tag on product pages.

One Response

I nee play later emi