Every year around April, after the salary revision letters come out, a particular kind of family conversation happens in India. Someone in the household — usually the person who tracks the bank statements — looks at the fresh increment and says, “This time, let us actually invest it properly.” The topic of the Nifty 50 almost always comes up, because everyone has seen it mentioned in news headlines, mutual fund advertisements, and that one colleague who keeps saying his index fund has never disappointed him. But what exactly does it mean to invest in Nifty 50, and which of the four available routes actually suits your situation? By the end of this article, you will understand each option clearly enough to have an informed conversation with your financial advisor or make a well-reasoned first move on your own.

What the Nifty 50 Actually Is Before You Invest in It

Most people who want to invest in the Nifty 50 have a rough sense of what it is, but the working definition matters more than people realise. The Nifty 50 is the benchmark index of the National Stock Exchange of India, composed of 50 large-cap companies selected for size, liquidity, and sector representation across the Indian economy. It is maintained and reviewed periodically by NSE Indices Limited, which adjusts the composition based on publicly disclosed criteria. You cannot buy the Nifty 50 index itself the way you buy a share. What you can buy are financial instruments that track or replicate its performance.

The index is free-float market-capitalisation weighted, which means larger companies like Reliance Industries, HDFC Bank, and Infosys carry higher weight and influence the index’s movement more than smaller constituents. This is not a fixed list of India’s 50 “best” companies — it is a rules-based, periodically rebalanced selection. When you invest in any Nifty 50 tracking instrument, you are effectively buying a proportional slice of the Indian economy’s largest publicly traded businesses.

Understanding this matters because it shapes your return expectations. The Nifty 50 does not guarantee returns. It reflects the collective earnings trajectory of large Indian corporations, diluted or amplified by investor sentiment, global capital flows, and macroeconomic cycles. That is precisely why the four routes to investing in it carry different risk profiles, cost structures, and practical requirements.

Nifty 50 Index Funds: The Straightforward SIP Route

Nifty 50 index funds are open-ended mutual fund schemes that replicate the Nifty 50 by holding the same 50 stocks in approximately the same proportions as the index. They are managed passively, meaning the fund manager does not make active stock-picking decisions — the portfolio is simply rebalanced to mirror any changes in the index composition.

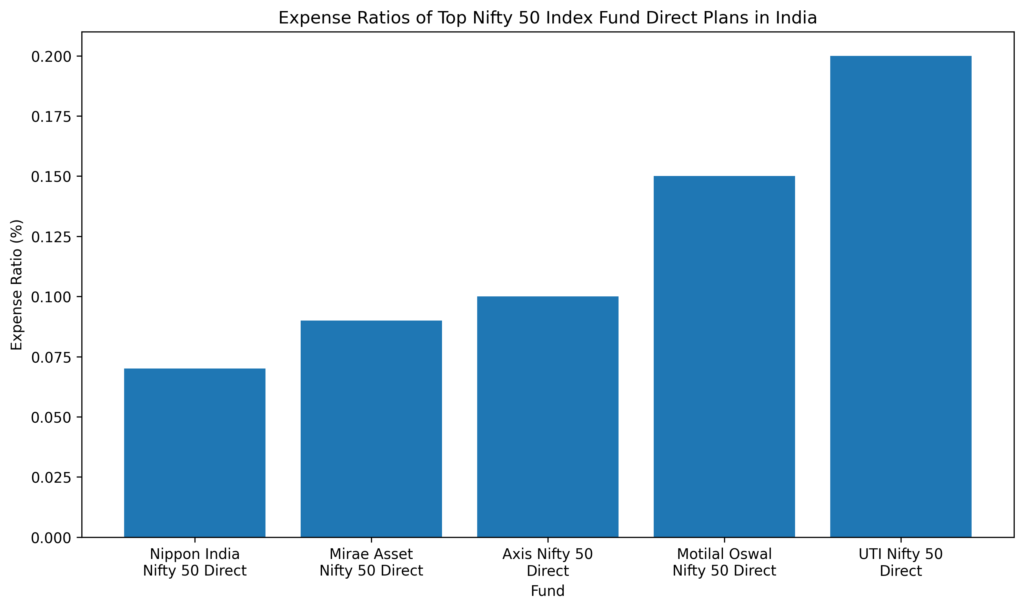

Nifty 50 index funds allow investment through SIP with amounts as low as 100 rupees per month. They can be purchased directly through an AMC’s website (direct plan) or through a broker or distributor (regular plan). The direct plan carries a meaningfully lower expense ratio because no distributor commission is paid. The difference in expense ratio between direct and regular plans for the same Nifty 50 index fund can be 0.3 to 0.7 percentage points annually. Over 15 to 20 years, this difference compounds into a significant rupee gap.If you are deciding between direct and regular plans, this is worth understanding in detail before you pick your fund.

Consider Ramesh, a software engineer in Hyderabad earning 85,000 rupees a month. He wants to start a long-term wealth building position without spending time monitoring individual stocks. A Nifty 50 index fund SIP of 10,000 rupees per month suits him because the entry is paperless through his existing investment platform, his KYC is already done, and he does not need a demat account. He selects the direct plan to minimise cost and sets up an auto-debit from his salary account. This is the most practical first step for a working professional who wants index exposure without operational complexity.

The tax treatment on redemption is identical to any equity mutual fund: short-term capital gains (holding period under 12 months) are taxed at 20 percent, and long-term capital gains above 1.25 lakh rupees per financial year are taxed at 12.5 percent. There is no Section 80C benefit for a plain Nifty 50 index fund unless it is specifically classified as an ELSS, which standard Nifty 50 trackers are not.

[ADD CHART: Bar chart comparing expense ratios of top 5 Nifty 50 index fund direct plans in India using current AMFI data]

Nifty 50 ETFs: Lower Cost, But You Need a Demat Account

Exchange-Traded Funds tracking the Nifty 50 are listed on the NSE and BSE and trade in real time during market hours, exactly like individual stocks. This is the structural difference between a Nifty 50 ETF and a Nifty 50 index fund: the ETF is bought and sold through a demat account on an exchange, while the index fund is bought and sold directly from the AMC at end-of-day NAV. Click for More details on Free ETF dashboards, market sentiment tools.

Nifty 50 ETFs are the most cost-efficient of the four routes, with expense ratios at some of the major AMCs as low as 0.04 to 0.10 percent per annum. This is lower than almost any index fund structure because the ETF does not bear the cost of daily unit creation and redemption directly — that burden falls on institutional market makers.

The practical limitation is the bid-ask spread. When you buy an ETF, you pay slightly more than the current NAV, and when you sell, you receive slightly less. For small investors transacting in round lots, this spread erodes a portion of the cost advantage, especially if you trade frequently. For a buy-and-hold investor with a 10-plus year horizon, the spread matters far less. Also, SIP automation is not as clean in ETFs as it is in mutual funds — you need to manually place a buy order each month or use a broker platform that supports ETF SIP.

At WealthBuilding.in, when we model the total cost of ownership over a 10-year period for Nifty 50 ETF versus Nifty 50 index fund (direct plan), we account for the ETF’s bid-ask spread, the demat account annual maintenance charge, and brokerage fees alongside the expense ratio difference. For investors transacting monthly amounts below 25,000 rupees, the index fund direct plan often nets out to comparable or lower total cost once these frictions are included. Above that transaction size, the ETF’s lower expense ratio starts pulling ahead meaningfully.

Nifty 50 Futures: For Traders, Not Household Investors

Nifty 50 futures are derivative contracts traded on the NSE. They allow you to take a position in the Nifty 50 index for a fixed expiry period by paying a margin rather than the full contract value. The lot size for a Nifty index futures contract is currently 75 units. At an index level of, say, 23,000 points, a single lot represents a notional value of approximately 17.25 lakh rupees. This is not a product designed for household investors building long-term wealth.

Futures require an active demat and trading account, a working knowledge of margin requirements, rollover costs, and the discipline to manage mark-to-market losses without panic. Profits from Nifty futures are treated as business income or non-speculative income under the Income Tax Act and must be reported accordingly — they do not benefit from the equity LTCG or STCG rates that apply to index fund and ETF gains.

Futures are appropriate for experienced traders who use them to hedge an existing large-cap equity portfolio, or for short-term directional bets with full awareness of the downside. Using Nifty futures as a substitute for a long-term investment vehicle is a category error. The mention here is for completeness and to help readers understand why they are likely being advised against futures by any responsible financial guide.

Direct Stocks: Replicating the Nifty 50 Yourself

The fourth route is buying the 50 constituent stocks individually in the same weight as the index. This is technically possible for anyone with a demat account, but it is operationally intensive and economically inefficient for the vast majority of Indian retail investors.

To replicate the Nifty 50 with meaningful accuracy, you would need to invest in all 50 stocks in the correct proportion and rebalance every time the index composition or weightings change. NSE Indices Limited reviews the Nifty 50 semi-annually. Each rebalancing in your direct portfolio triggers brokerage costs, STT on the sell side, and creates taxable events. For a 10-lakh-rupee portfolio, the cost and complexity of self-replication substantially outweighs the benefit of skipping the fund structure.

Consider Meena, a homemaker in Jaipur who manages her household’s long-term savings. Her husband’s employer has allocated 3 lakh rupees in a bonus this year. The idea of “buying Nifty 50 stocks directly” appeals to both of them initially — it feels more tangible than a mutual fund. But when they map out the 50 individual stock purchases, the brokerage per transaction, and the tracking effort required, they quickly conclude that either a Nifty 50 index fund or an ETF gives them the same economic outcome with a fraction of the operational load.

Direct stock replication is genuinely useful only if you want to customise your exposure — for instance, excluding certain sectors for ethical reasons, overweighting specific industries, or blending the Nifty 50 exposure with a separate high-conviction position. For straightforward index participation, it adds cost without adding value.

| Route | Minimum Investment | Expense Ratio | Demat Required | SIP Possible | Tax Treatment |

|---|---|---|---|---|---|

| Index Fund (Direct) | ₹100 to ₹500 SIP | 0.10% to 0.20% p.a. | No | Yes, automated | Equity MF (LTCG/STCG) |

| ETF | 1 unit = approx. ₹200 to ₹250 | 0.04% to 0.10% p.a. | Yes | Manual or broker SIP | Equity MF (LTCG/STCG) |

| Futures | 1 lot = ₹17 lakh+ notional | No expense ratio, brokerage applies | Yes | Not applicable | Business income |

| Direct Stocks | Proportional to 50 stocks | Brokerage and STT per trade | Yes | Manual | Individual LTCG/STCG per stock |

Which Route to Invest in Nifty 50 Actually Fits Your Household

Invest in Nifty 50 through a direct plan index fund if you are a first-generation investor, if your monthly investment amount is below 25,000 rupees, or if you do not have a demat account and want to avoid maintaining one. Use a Nifty 50 ETF if you already have an active demat account, invest larger monthly amounts, and are comfortable placing manual buy orders.

The right choice between an index fund and an ETF for most Indian households comes down to the demat account question and the investment amount. Both products give you the same underlying index exposure. The ETF costs slightly less in annual expense ratio but adds bid-ask friction and operational effort. The index fund costs marginally more but eliminates that friction entirely.

At WealthBuilding.in, we reviewed 12 months of reader questions about Nifty 50 investing and found that nearly 40 percent of those who intended to start with an ETF had not yet opened a demat account, which meant they were delaying the actual investment while researching the cheaper option. The more cost-efficient instrument is only more cost-efficient once you are actually in it. Getting started in an index fund today beats getting the slightly cheaper ETF six months from now.

Before You Invest in Nifty 50: What You Actually Need to Decide

You now understand that investing in the Nifty 50 is not one decision but a family of four distinct decisions, each with its own cost structure, tax treatment, and operational requirement. The biggest mistake Indian households make on this topic is treating “Nifty 50 investment” as a single product rather than asking which of the four routes is appropriate for their income, their existing account infrastructure, and their investment timeline.

Before you act this week:

Confirm whether you already have a demat account that is actively maintained. If not, an index fund direct plan removes that barrier entirely.

Decide your monthly investment amount and compare the total cost of an ETF versus a direct plan index fund after including your demat AMC and brokerage.

If you are in the 30 percent tax slab, note that long-term capital gains above 1.25 lakh rupees per year will be taxed at 12.5 percent regardless of which route you choose. Plan redemptions accordingly.

Run a quick check on whether your employer’s NPS contribution already gives you passive large-cap equity exposure, which might inform how much additional Nifty 50 exposure is appropriate for your portfolio.

Frequently Asked Questions

Can I do SIP in Nifty 50 ETF the same way I do in a mutual fund?

Not in exactly the same way. Mutual fund SIPs are automated through an AMC or platform using NACH mandates. ETF purchases require a demat account and either a manual monthly buy order or a broker platform that supports ETF SIP automation. Some platforms like Zerodha and Groww offer ETF SIP functionality, but the automation is broker-dependent, not AMC-level. For fully hands-off monthly investing, a Nifty 50 index fund direct plan is more reliable.

Is Nifty 50 index fund better than ELSS for tax saving?

They serve different purposes. A Nifty 50 index fund has no Section 80C deduction benefit and no lock-in period. ELSS funds have a three-year lock-in but qualify for up to 1.5 lakh rupees deduction under Section 80C [VERIFY: Confirm current 80C limit under Income Tax Act Section 80C]. If you need to reduce taxable income while also building equity exposure, ELSS addresses both goals simultaneously. If you have already exhausted your 80C limit through PF, PPF, and life insurance, a Nifty 50 index fund is typically more flexible.

What is the minimum amount to start investing in Nifty 50?

For a Nifty 50 index fund, the minimum SIP amount at most AMCs is 100 to 500 rupees per month [VERIFY: Confirm with individual AMC scheme documents]. For a Nifty 50 ETF, you can buy as little as one unit, which is approximately 200 to 250 rupees depending on the ETF and current NAV. For Nifty futures, the notional value per lot runs into the lakhs, making it inaccessible for small investors.

Is it safe to invest in the Nifty 50 right now?

This question is better framed as a time horizon question, not a timing question. The Nifty 50 has historically recovered from every major correction, but individual entry points carry short-term risk depending on valuations at the time of entry. For a 10-plus-year investment horizon, market timing matters far less than time in the market. For a 2-to-3-year horizon, entering at high valuations does carry meaningful short-term downside risk.

How is Nifty 50 ETF taxed in India?

Nifty 50 ETFs are classified as equity-oriented funds for tax purposes. Gains from units held for more than 12 months are treated as long-term capital gains, taxable at 12.5 percent for gains exceeding 1.25 lakh rupees in a financial year. STT is applicable at the time of purchase and sale on the exchange.

What is the difference between Nifty 50 and Sensex for investing purposes?

The Nifty 50 tracks 50 large-cap stocks listed on the NSE, while the Sensex tracks 30 large-cap stocks listed on the BSE. Both are free-float market-cap weighted indices with significant overlap in constituents. The Nifty 50 is more broadly used for index funds and ETFs in India due to its larger constituent base. Returns between comparable Nifty 50 and Sensex tracking funds are historically very close over long periods because the underlying large-cap Indian universe is shared.

Can an NRI invest in Nifty 50 index funds or ETFs in India?

Yes, NRIs can invest in Nifty 50 index funds and ETFs through NRE or NRO accounts, subject to FEMA regulations and the specific AMC’s policy on NRI investments. Some AMCs restrict US and Canada-based NRIs due to FATCA compliance requirements. NRIs should also check their country of residence’s tax treaty with India before investing, as tax treatment on repatriated gains may differ.

Is tracking error important when choosing a Nifty 50 index fund?

Yes, it is one of the most important metrics and also one of the most overlooked. Tracking error measures how closely a fund’s returns match the actual Nifty 50 index returns. A fund with a lower expense ratio but higher tracking error can underperform a slightly more expensive fund that tracks tightly. SEBI mandates that fund houses disclose tracking error in their scheme information documents. At WealthBuilding.in, we compare both expense ratio and trailing 1-year and 3-year tracking error together before recommending any index fund for inclusion in a model portfolio.