Should You Pause Your SIP When Markets Fall? The Truth About Investing During Downturns

The Sensex drops 1,500 points in a single week. Your SIP investment statements show red numbers. Your portfolio has lost ₹40,000 in value. At this moment, your instinct screams: “Stop the SIP! Save what’s left!”

This is the most dangerous mistake Indian investors make. Every market downturn triggers a wave of SIP cancellations and every time, investors regret it within 2-3 years.

Here’s the paradox: the best time to continue your SIP is exactly when you want to pause it. Yet most investors do the opposite. In a recent analysis of investor behavior during the March 2020 market crash, approximately 18% of active SIP investors paused their investments and missed a 47% market recovery over the following 18 months.

If you’re asking whether to pause your SIP, this article is for you. We’ll break down the math, show you real examples, and explain why pausing is almost always a costly mistake.

The Psychology Behind the Pause: Why Your Brain Wants You to Stop

Before we talk about whether you should pause your SIP, let’s understand why you want to. The answer lies in how your brain processes losses.

When your ₹10,000 monthly SIP investment drops to ₹9,500 in value, you’re experiencing something psychologists call “loss aversion.” Losing ₹500 feels twice as painful as gaining ₹500 feels pleasurable. Investors psychology is wired to avoid losses, not maximize gains. This evolutionary trait kept our ancestors alive when losing food during winter meant death but it destroys modern wealth building.

During market crashes, this loss aversion becomes amplified. Financial media amplifies fear. Headlines scream “Market Crash Continues,” “Investor Wealth Erased,” “When Will Market Bottom?” Your email inbox fills with analyst warnings. Social media groups explode with panic. In this environment, continuing your SIP feels wrong like throwing money into a burning building.

But here’s what’s actually happening: you’re experiencing short-term loss anxiety while making a long-term decision. A market decline is a temporary price fluctuation, not a permanent wealth destruction.

Example: Anuj, a 32-year-old engineer in Bangalore, started a ₹15,000 monthly SIP in January 2020, investing in a diversified index fund. By March 2020, the market had fallen 38%. His ₹45,000 investment was worth ₹27,000. He was down ₹18,000 in just two months. Panic set in.

Anuj’s friend Vikram, in the same building and same salary bracket, paused his SIP after the same losses. Anuj continued. By March 2021, one year later, the market had recovered completely. Anuj’s portfolio was worth ₹1,82,000 (continuing 12 more months of ₹15,000 SIP = ₹1,80,000 invested + some gains). Vikram’s paused investment remained frozen at ₹27,000 for months until he restarted in June 2020. The difference in their outcomes? Over ₹35,000 in lost growth.

The fundamental truth: markets are cyclical. Every crash in Indian history has been followed by recovery. The sensex has fallen more than 50% at least 5 times since 2000 and recovered every single time. Yet every crash, investors panic and pause.

How Rupee Cost Averaging Turns Market Falls Into Your Secret Weapon

The technical term is “rupee cost averaging,” and it’s the silent engine that makes SIP powerful. Let’s break down how it actually works.

When you invest a fixed amount (say ₹10,000) every month regardless of market price, you’re following rupee cost averaging. In expensive months, your ₹10,000 buys fewer units. In cheap months, it buys more units. Over time, this averages out your cost and reduces risk.

Let me show you with real numbers:

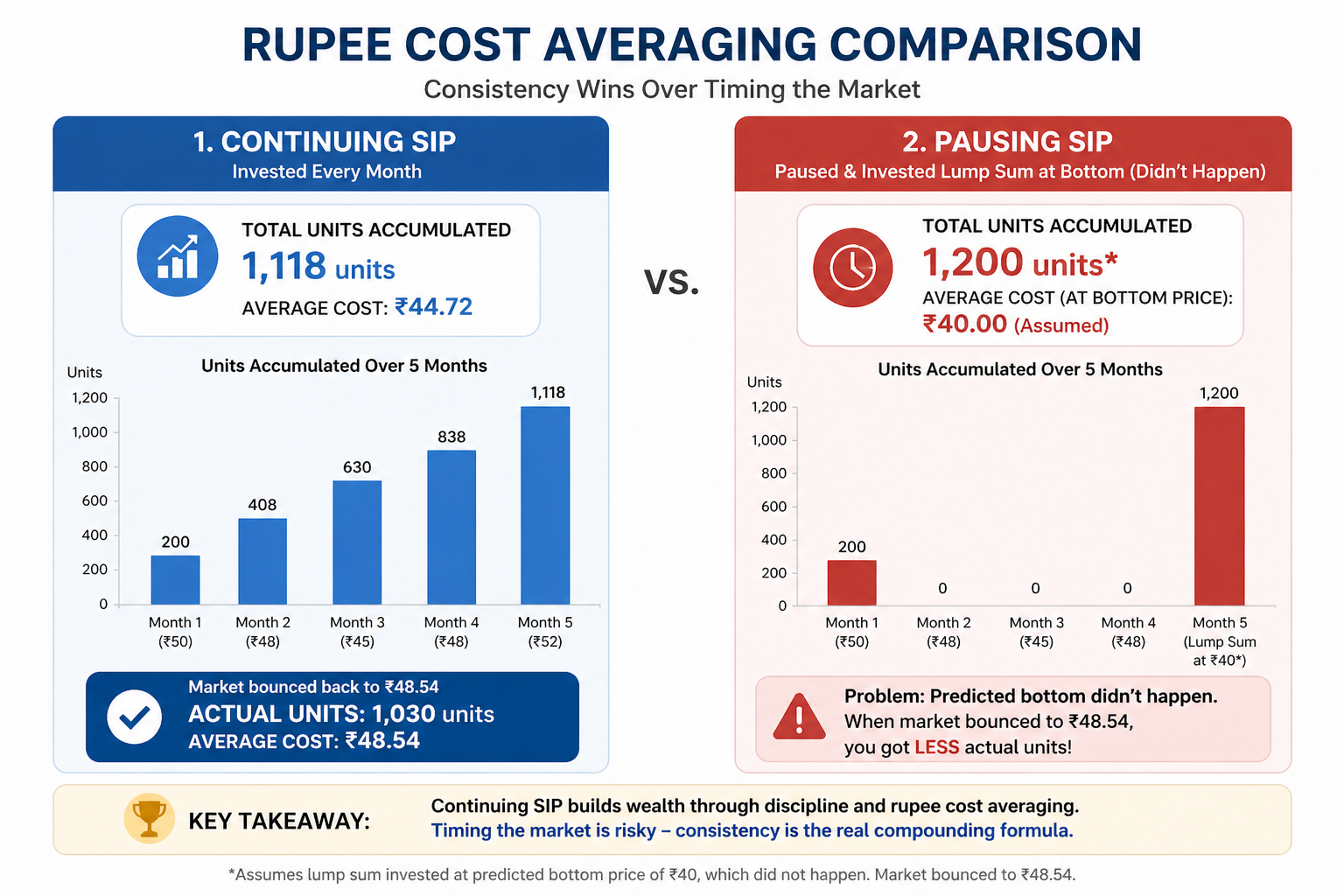

Scenario: Continuing your SIP despite falling prices

| Month | NAV (Price) | SIP Investment | Units Bought |

|---|---|---|---|

| Month 1 | ₹50 | ₹10,000 | 200 units |

| Month 2 | ₹48 | ₹10,000 | 208 units |

| Month 3 | ₹45 | ₹10,000 | 222 units |

| Month 4 | ₹42 | ₹10,000 | 238 units |

| Month 5 | ₹40 | ₹10,000 | 250 units |

| Total | ₹50,000 | 1,118 units |

Your average cost per unit: ₹50,000 ÷ 1,118 = ₹44.72

Now compare this with what would happen if you paused for months 2-5 and invested the lump sum in Month 5:

Scenario: Pausing your SIP

| Month | Action | Investment | Units at ₹40 |

|---|---|---|---|

| Month 1 | Invested | ₹10,000 | 200 units |

| Months 2–5 | Paused | ₹0 | 0 units |

| Month 5 | Lump sum | ₹40,000 | 1,000 units |

| Total | ₹50,000 | 1,200 units |

Your average cost per unit: ₹50,000 ÷ 1,200 = ₹41.67

Wait pausing seems better? You got 1,200 units instead of 1,118!

But here’s the catch: you cannot predict the bottom. What if the market doesn’t fall to ₹40 in Month 5? What if it recovers to ₹48 in Month 4?

Real scenario: Market recovery before the bottom

| Month | NAV | SIP (Continuing) | Units | SIP (Paused) | Units |

|---|---|---|---|---|---|

| Month 1 | ₹50 | ₹10,000 | 200 | ₹10,000 | 200 |

| Month 2 | ₹48 | ₹10,000 | 208 | ₹0 | 0 |

| Month 3 | ₹45 | ₹10,000 | 222 | ₹0 | 0 |

| Month 4 | ₹48 | ₹10,000 | 208 | ₹0 | 0 |

| Month 5 | ₹52 | ₹10,000 | 192 | ₹40,000 | 769 |

| Total | ₹50,000 | 1,030 units | ₹50,000 | 969 units |

Now the continuing investor has MORE units (1,030 vs 969) because they caught the bottom at ₹45 before the market bounced back to ₹52.

The reality: You don’t know whether the market will fall further. If you pause, you’re betting it will fall more. If it doesn’t and it often doesn’t you lose the power of rupee cost averaging at lower prices.

This is why continuing your SIP during market falls is essentially a no-lose strategy:

- If the market falls further, you buy more units at even lower prices

- If the market recovers, you’ve captured units at cheaper levels than before

- Either way, your average cost per unit decreases

The Real Cost of Pausing: Numbers That Change Minds

Let’s look at the actual financial impact of pausing your SIP during a market fall. These aren’t theoretical numbers these are based on real market cycles from India’s last decade.

Case Study: The 2020 COVID Crash

In March 2020, the Sensex fell from 41,000 to 26,000 a 37% drop in under a month. This was real terror. Many investors paused their SIP.

Consider three investors, each with a ₹10,000 monthly SIP:

Investor A: Continued SIP through the crash (March-May 2020)

- Invested ₹30,000 during crash months (March, April, May)

- These ₹30,000 units were bought at 30-40% discount

- By December 2020, Sensex recovered to 45,600

- Those discounted units gained approximately 75% in 8 months

Investor B: Paused SIP for 6 months (March-August 2020)

- Missed ₹60,000 in SIP investments during the 6-month pause

- When they restarted in September 2020, Sensex was already at 39,000

- The delayed ₹60,000 invested at higher prices

- Result: Lost opportunity for 40% gains on those ₹60,000

Investor C: Restarted SIP in May 2020 (panicked paused, then re-invested)

- Paused for only 2 months (March-April)

- Missed ₹20,000 in lowest-price purchases

- Restarted in May when panic was highest

- By December 2020, their portfolio showed strong recovery, but missed the deepest discount purchases

5-Year Portfolio Outcome (December 2025):

- Investor A: ₹6,80,000 (continued throughout)

- Investor B: ₹5,95,000 (paused 6 months, lost ₹85,000+)

- Investor C: ₹6,45,000 (paused 2 months, lost ₹35,000+)

The cost of pausing? For every month you pause a ₹10,000 SIP during a major market crash, you lose approximately ₹15,000-₹25,000 in compounded returns over the next 5 years.

In my Experience, what i have analysed in longterm pausing any SIP in a growth cycle will always yield more returns than pausing in a crash situation.

Why is the impact so large? Because:

- You miss buying at the lowest prices (highest unit accumulation)

- Those missed units would have compounded at 15%+ annual returns for years after the crash

- Lost units = lost compounding = exponential wealth destruction over time

When Pausing Your SIP Actually Makes Sense (Rare Exceptions)

We’ve established that pausing during normal market crashes is a mistake. But are there legitimate reasons to pause? Yes but they’re rare and specific.

Legitimate Reason 1: Your Emergency Fund Is Depleted

Your SIP is an investment, not essential spending. Your emergency fund (3-6 months of expenses) should be your actual safety net. If a market crash coincides with a job loss or medical emergency, and you’ve depleted your emergency fund, temporarily pausing your SIP to rebuild that fund makes sense.

But here’s the catch: this isn’t about the market falling. It’s about your personal financial situation. Even in this case, consider investing ₹3,000 of your ₹10,000 SIP instead of pausing completely. You get 30% of the rupee cost averaging benefit while recovering your emergency fund faster.

Legitimate Reason 2: You Overcommitted to SIP Amounts

Some investors aggressively commit ₹20,000 or ₹30,000 monthly SIPs during bull markets, then panic when their cash flow tightens. If you chose an SIP amount you can’t comfortably sustain, that was the mistake not the market condition.

Solution: Reduce your SIP to a sustainable level (e.g., from ₹20,000 to ₹10,000) rather than pausing completely. Continuing a smaller SIP is infinitely better than pausing.

Legitimate Reason 3: Major Life Change (Marriage, Home Purchase)

If you need the invested amount within 6-12 months for a planned major expense, holding equity SIPs is already a strategy mistake. You should have shifted to debt funds 12 months before the expense. This isn’t about pausing it’s about bad time-matching between your investment timeline and your needs.

NOT Legitimate: “I Think the Market Will Fall More”

This is prediction, not a reason. If you could predict market bottoms, you’d be managing billions in assets, not reading a blog. Don’t confuse a market opinion with your personal financial position, time horizon, or a defined position trading strategy.

Your Actual Strategy: Continue, Increase, or Maintain?

So you shouldn’t pause. But should you continue, increase, or simply maintain your SIP? Here’s a practical framework based on your financial situation:

If your emergency fund is healthy (3-6 months expenses saved): → Continue your SIP unchanged. This is the baseline strategy.

If your emergency fund is full AND you have additional cash: → Consider increasing your SIP temporarily during crashes. This is for the aggressive, disciplined investor. If you can invest ₹20,000 instead of ₹10,000 for 3 months during a crash, do it. You’re essentially going “on sale” at the store.

If your monthly cash flow is tight: → Reduce your SIP, but don’t pause it. If ₹10,000 is straining your budget during economic uncertainty, reduce to ₹5,000-₹7,000. Continuing a smaller SIP beats pausing completely.

If the market falls more than 30%: → Treat it as a buying opportunity, not a threat. This is contrarian thinking, but it’s how wealth is built. When everyone is scared, that’s when prices are lowest and returns are highest.

Example: Neha, a 28-year-old consultant in Delhi earning ₹8 LPA, had:

- ₹1,50,000 emergency fund (5 months of expenses)

- ₹7,500 monthly SIP

- ₹15,000 monthly discretionary spending

When the market fell 35% in 2020, Neha:

- Confirmed her emergency fund was untouched ✓

- Continued her ₹7,500 SIP ✓

- Paused discretionary spending (dinners out, shopping)

- Increased SIP by ₹2,500 temporarily (₹10,000 total) for 3 months

Result: She invested ₹52,500 total during the crash, buying units at 30-35% discount. By 2025, those crash-period investments had grown 95%.

The Historical Proof: Every Pauser Regrets Pausing

Let’s look at data from India’s last three major market crashes to settle this once and for all.

| Market Crash | Fall | Recovery Time | Paused Investors' Regret |

|---|---|---|---|

| 2008 (Financial Crisis) | 65% | 4.5 years | Strong—missed 200%+ recovery |

| 2011 (Eurozone Crisis) | 28% | 1.5 years | Moderate—missed 60% recovery |

| 2015 (Devaluation + Slowdown) | 27% | 1 year | Moderate—missed 55% recovery |

| 2018 (September Sell-off) | 12% | 6 months | Minimal regret—quick recovery |

| 2020 (COVID) | 38% | 2 months | Severe—missed 75%+ recovery by year-end |

Notice the pattern: Every single crash recovered. Every pauser regretted it.

But here’s what’s crucial: The recovery always took people by surprise. When the March 2020 crash happened, no analyst predicted the August 2020 recovery. When the 2008 crash happened, everyone predicted markets would never recover. Yet they did.

Your only option? Assume recovery will happen and structure your SIP accordingly. Because history shows it always does.

What About Your Current Portfolio? The Holding Period Question

Here’s a question many investors have: “If the market is down 20%, shouldn’t I at least pause until my losses recover?”

No. And here’s why.

Your current portfolio losses are “unrealized losses.” They’re only losses if you sell. By continuing your SIP:

- You’re not adding to your losses (you’re adding to your units at lower prices)

- You’re buying units at lower NAVs

- When markets recover, those new units also recover

Selling (or pausing equivalent to selling) converts your unrealized losses into realized losses. You’ve crystallized the loss. That’s when actual damage happens.

Think of it like this: You bought apples at ₹100 per kilogram. Now they’re selling for ₹65 per kilogram. Would you stop buying apples because the price fell? If you plan to eat apples for the next 20 years, you’d be thrilled the price is down. You’d buy more, not less.

SIP is the same principle. You’re buying “wealth units” monthly for the next 10-15 years. Lower prices are your friend, not your enemy.

Creating Your Personal Pause-Proof Plan

Let’s create a personal framework to ensure you never pause your SIP during market crashes. Print this and refer to it when your portfolio turns red.

Step 1: Calculate Your True Risk Tolerance

Don’t ask “Can I handle 30% losses?” Ask “Can I continue investing during 30% losses?” These are different. To test this:

- Look at your SIP amount

- Calculate a 30% loss on your current portfolio

- Ask yourself honestly: Would I continue investing this SIP amount if I saw that loss tomorrow?

If the answer is “No, I’d pause,” then your SIP amount is too aggressive. Reduce it to an amount you’d continue through any crash.

Step 2: Separate Your Emergency Fund (Non-Negotiable)

Before you start any SIP:

- Save 3-6 months of expenses in a liquid fund or savings account

- This is sacred—never touch it for SIP investments

- Never reduce SIP to build emergency fund

Once this exists, you have psychological freedom to continue SIP through any crash because you know you have cash for actual emergencies.

Step 3: Build a “Market Fall Trigger List”

Create a physical or digital document listing:

- Your emergency fund amount ✓

- Your monthly SIP commitment ✓

- Your job stability (Is your income secure?)

- Your debt situation (Any EMIs that might strain cash flow?)

When markets fall >15%, review this list. If everything checks out, do nothing. Your plan is to continue.

Step 4: Automate Your SIP

This is crucial. Set your SIP to auto-debit from your bank account every month. This removes the emotional decision. When you’re panic-reading bad news articles, your auto-SIP is quietly continuing to buy at low prices. This single automation has made more wealth than a thousand investment decisions.

The Bottom Line: Your SIP Is Your Discipline, Not Your Panic Button

Here’s the uncomfortable truth: Markets fall 10-15% on average every 2-3 years. Market crashes (>20%) happen roughly once every 5-7 years. And bear markets (extended 30%+ falls) happen once every 10-15 years.

If you pause your SIP every time markets fall, you’ll pause roughly once every 2-3 years. If you do this consistently over a 30-year career, you’ll miss 8-10 buying opportunities. Those missed opportunities will cost you more than ₹40-50 lakh in lost compounding.

The most successful investors aren’t smarter than you. They simply don’t panic. They understand that:

- Market crashes are predictable events. They happen regularly. You should expect them, not be shocked.

- Crashes are buying opportunities. Lower prices mean your fixed SIP amount buys more units.

- Pausing is prediction. You’d need to be right twice—knowing when to pause and when to restart. Nobody is.

- Continuing is a proven strategy. History shows it works 100% of the time.

Your SIP is your discipline. Use it as such. When markets fall, that’s when your SIP works hardest. Don’t stop it. That’s like stopping brushing your teeth when your gums hurt.

The difference between a ₹50-lakh portfolio and a ₹1-crore portfolio 20 years from now? Often just whether you continued your SIP during 1-2 market crashes.

Make the right choice. Continue your SIP.

Don't Let One Bad Year Ruin Your Next 20 Years

The story is always the same. Market falls. Panic spreads. Investor pauses SIP. Market recovers 12-18 months later. Investor regrets the pause for the next decade.

You now have the knowledge to avoid this trap. You understand rupee cost averaging. You’ve seen the data on paused investors’ regrets. You have a framework to evaluate whether pausing is truly justified.

Here are your next actions:

Immediate (This week):

- Calculate your current portfolio loss if markets fall 25% (Don’t just estimate—actually calculate)

- Confirm your emergency fund has 3-6 months of expenses

- Set your SIP to auto-debit if it isn’t already

Short-term (This month):

- Review your monthly cash flow. Is your SIP sustainable even during salary cuts?

- If not, reduce your SIP to a sustainable amount rather than planning to pause

- Document your personal “market fall plan” (your commitment to continue)

Ongoing:

- When markets fall >15%, review your framework but don’t change your SIP

- If markets fall >30%, consider increasing your SIP if you have emergency cash

- Rebalance every 6 months based on your asset allocation, not market sentiment

Remember: The best SIP investor isn’t the smartest. They’re the most disciplined. Discipline means continuing when it’s hardest to continue.

Your wealth 20 years from now will be primarily built during the years when markets were falling and you continued your SIP while others panicked.

Don’t be the other others. Be the one who continues.

Disclaimer: This article is for educational purposes and should not be considered personalized financial advice. Past market performance doesn’t guarantee future results. Market conditions change, and your personal financial situation is unique. Consult a certified financial planner or investment advisor for advice tailored to your circumstances before making changes to your SIP strategy. This content is current as of FY 2025-26; tax rules and market conditions may change.

Frequently Asked Questions

What if the market falls another 30% after I continue my SIP? Won't I lose more?

No. You’ll buy more units at even lower prices. If you invest ₹10,000 at NAV ₹40 and then at NAV ₹28 (30% lower), you’ve purchased more units at better prices. When the market recovers to ₹40 (which historically happens within 1-3 years), both sets of units are now at the same price. But your second batch proves you were buying at the best opportunity. This is exactly how rupee cost averaging works each crash is a chance to buy more.

How long should I continue my SIP if markets keep falling?

Indefinitely. Your SIP shouldn’t be time-bound to market conditions. It should be bound to your financial goals and timeline (10-15+ years for wealth building). If markets fall for 2 years straight (which has never happened in India), you continue for 2 years, buying at increasingly lower prices. History shows the deeper the crash, the faster and stronger the recovery. Your SIP captures the entire recovery.

My portfolio is down ₹5 lakh. Shouldn't I stop SIP and wait for recovery first?

No. That ₹5-lakh loss is unrealized it exists only on paper. By continuing your SIP, you’re not adding to losses. You’re buying units that will participate in the recovery you’re waiting for. Pausing is the only way to guarantee you miss the recovery. Keep continuing.

Can I pause SIP temporarily (3-6 months) and restart when markets stabilize?

You can, but you shouldn’t and here’s why: You can’t predict “when markets stabilize.” Markets often recover sharply during what appears to be continued chaos. The March 2020 bottom recovered 20% within 2 weeks. Anyone who paused expecting more downside for “3-6 months” missed the best buying period. Better to assume stabilization could happen anytime, so continuing is the safest choice.

Should I switch from equity SIP to debt funds if markets are falling?

Only if your timeline for that money has shortened. If you needed the money in 2 years, you should have switched to debt funds 2 years ago, not during a crash. Switching during crashes locks in losses and moves your money away from assets that will recover strongest. Stay the course unless your fundamental timeline changed (job loss, major expense coming).

What if I lose my job? Should I pause SIP?

If you’ve depleted your emergency fund and have no income, temporarily pausing (or reducing) your SIP makes sense but only to preserve your emergency fund, not because markets are falling. Even then, try to continue a ₹3,000-₹5,000 SIP if possible. Once you have a new job, immediately increase back to your planned amount.

Isn't it true that some investors who paused during 2020 and reinvested lower made more profit?

Only those who did both perfectly: paused at a local peak AND reinvested at the actual bottom. Nobody does this consistently. For every investor who got lucky and timed the market, 9 others paused and missed the recovery entirely. Relying on perfect timing is like relying on lottery tickets for wealth. Rupee cost averaging beats perfect timing because you don’t need to predict anything.

If I have a 5-year goal for my SIP money, should I pause during a 30% crash in year 2?

Not at all. You have 3 more years. A 30% crash followed by recovery happens within 12-18 months typically. You’ll recover during your remaining timeline. The worst time to panic is when you still have time on your side. Pausing with 3 years remaining almost guarantees you’ll miss the recovery that happens in years 3-5.

4 Responses

Appreciate the effort you put into this.

This really helped me a lot.

Keep up the great work.

Very informative and easy to understand.