Suresh, a 34-year-old LIC agent in Nashik, sold his first ₹50,000-premium endowment policy in October 2024 expecting the same payout his senior colleagues had been quoting him for years. The cheque was smaller than he expected — and a slightly larger one followed the next year. Nobody had told him that LIC quietly rewrote its own commission structure that very month.

If you’re a self-employed insurance agent, or about to become one, this confusion is common. Most commission charts circulating online are copies of 2016-era tables that no longer apply. The commission structure for a LIC agent in India changed fundamentally after IRDAI scrapped fixed, product-wise commission caps in 2023, and LIC itself revised its first-year-to-renewal split again in October 2024. This article walks through exactly how your commission is built today, layer by layer, with real numbers, so you know what to expect from your very first policy onward.

(If you’re still deciding whether to become a LIC agent at all — eligibility, the IRDAI exam, licensing timeline — that ground is covered in our complete LIC agent guide. This article assumes you already know that part and want to understand the money mechanics.)

The Rule Change Most Agents Don't Know About

Until March 2023, every insurer in India operated under the IRDAI (Payment of Commission or Remuneration or Reward to Insurance Agents and Insurance Intermediaries) Regulations, 2016. That framework hard-capped commission product by product — a fixed ceiling baked into regulation, the same for every insurer selling a similar product.

From April 1, 2023, IRDAI replaced that entire approach with the IRDAI (Payment of Commission) Regulations, 2023. Product-wise caps disappeared. In their place, each insurer now follows a board-approved commission policy, constrained only by an overall Expense of Management (EoM) limit rather than a per-product percentage. This didn’t change LIC’s published rates on day one, but it gave LIC the legal room to revise them on its own schedule going forward — which it did.

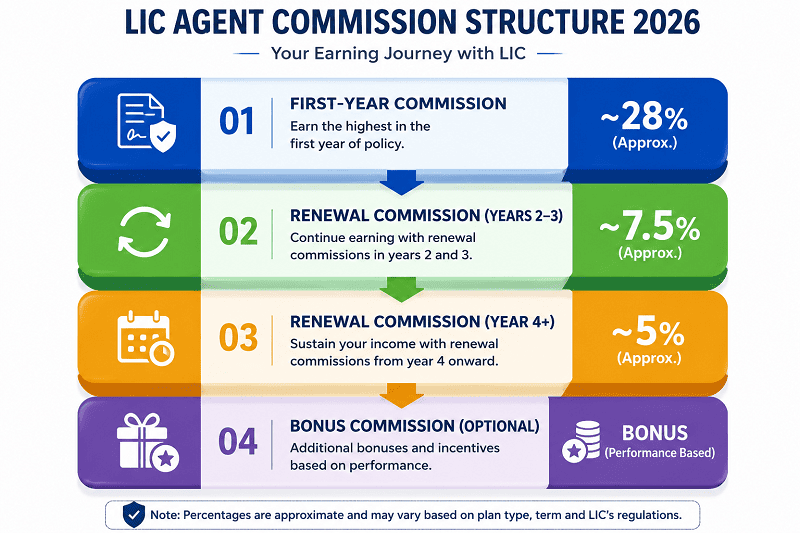

In October 2024, alongside new IRDAI rules requiring insurers to pay a higher guaranteed surrender value earlier in a policy’s life, LIC cut its first-year commission on many regular-premium plans from 35% to 28%, while raising the second-year-onward renewal commission from 5% to 7.5%. The logic: if the company has to set aside more money for early surrender value, less is available to front-load into a large first-year commission, so the balance shifted toward rewarding agents who keep customers paying year after year.

This is the single fact every new or self-employed LIC agent needs to internalize before relying on any commission number a recruiter or senior agent quotes verbally: the headline percentage they remember might be the pre-October-2024 rate, not the one your policies are actually being paid against today.

The Three Layers That Make Up Your Commission

LIC agent commission isn’t one number — it’s three separate layers stacked on top of each other, and each layer behaves differently.

First-year commission is paid once, when a customer’s first premium is collected on a new policy. It’s the largest single payout you’ll see on any policy, and it’s where most of the variation between plan types lives.

Renewal commission is paid every year the customer keeps paying, but it isn’t flat. Most regular-premium plans pay one rate for years two and three, then a lower rate from year four onward for as long as the policy stays in force.

Bonus commission sits on top of the first-year base commission for many regular-premium plans, paid as an additional percentage of that first-year figure. It generally isn’t payable on single-premium products or on specific plan numbers LIC excludes from the bonus pool.

Here’s how the first two layers typically look across broad plan categories, based on LIC’s commission structure post the October 2024 revision:

| Plan Category | First-Year Commission | Renewal Commission (Years 2–3) | Renewal Commission (Year 4 Onward) |

|---|---|---|---|

| Regular-Premium Endowment / Whole-Life Plans (PPT 15+ Years) | ~25–28% | ~7.5% | ~5% |

| Regular-Premium Endowment / Whole-Life Plans (PPT Under 15 Years) | ~18–22% | ~7.5% | ~5% |

| Pure Term Insurance Plans | Slab-based by policy term, typically 5–25% | ~5–7.5% | ~5% |

| Money-Back & Children's Plans | ~20–25% | ~7.5% | ~5% |

| Pension / Annuity Plans | ~7.5% (lower for single-premium variants) | ~2% | ~2% |

| ULIPs (e.g., SIIP) | ~2–7%, weighted toward later years | ~3.5–4.5% | ~4.5–7% |

| Single-Premium Plans | One-time ~2% | Not Applicable | Not Applicable |

A Worked Example: What One Policy Actually Pays You Over Time

Take Suresh’s policy: a ₹50,000-annual-premium endowment plan with a 15-year-plus premium-paying term, sold after the October 2024 revision.

- Year 1: 28% of ₹50,000 = ₹14,000

- Years 2–3: 7.5% of ₹50,000 = ₹3,750 each year (₹7,500 total)

- Year 4 onward: 5% of ₹50,000 = ₹2,500 every year the policy stays in force

Add those up over the first five years and Suresh has earned ₹14,000 + ₹3,750 + ₹3,750 + ₹2,500 + ₹2,500 = ₹26,500 from one policy, against ₹2,50,000 of premium the customer has paid in over those five years. That’s a blended commission rate of roughly 10.6% across five years — a useful number to hold onto, because it’s far closer to what your real average payout looks like than the headline first-year percentage.

Now compare the same ₹50,000 premium sold on a policy with a premium-paying term under 15 years. The first-year commission band for that shorter term is typically lower — often in the 18–22% range instead of 25–28% — purely because LIC’s schedule rewards longer premium-paying terms with a higher first-year slab. Two customers paying an identical premium can generate meaningfully different first-year commission for the agent, depending only on how many years they agreed to pay. This is exactly why Development Officers train new agents to recommend the longest premium-paying term a client is comfortable with: it’s the one lever within a fixed-premium product that directly changes the agent’s first-year payout.

Bonus Commission, Persistency, and Club Grading — The Part Nobody Explains Clearly

Three separate things get lumped together under “LIC agent bonuses,” and conflating them leads to unrealistic income expectations.

Bonus commission is the additional layer on top of first-year base commission described above — a genuine commission addition, paid in cash, conditional on plan type.

Persistency isn’t a bonus at all, but it now matters more to your income than it did before October 2024. Because the renewal share rose from 5% to 7.5% in years two and three, a larger fraction of your total lifetime earnings from any single policy now depends on whether that customer keeps paying. An agent who writes ₹10 lakh of new business a year but loses half their book to lapses by year three earns meaningfully less than one writing the same ₹10 lakh with high persistency, even though both look identical on a first-year-commission report.

Club grading — Zonal Club, National Club, Chairman’s Club, and similar tiers — adds a separate uplift, typically a percentage addition on top of first-year commission for agents who cross specific premium and policy-count thresholds within a single business year, alongside the non-commission perks (foreign trips, enhanced medical cover) we’ve detailed in our complete LIC agent guide. The commission uplift itself is real, but reaches a minority of LIC’s lakhs-strong agent force in any given year — useful as a stretch target, not as a number to build your monthly budget around.

What You Actually Keep: TDS, GST, and the Tax Mechanics of Commission

Two deductions affect the commission figure your branch actually pays you, and one common belief about how you can file your return is incorrect.

TDS is governed by Section 194D of the Income Tax Act. From April 1, 2025, the rate for individuals dropped to 2% (from the earlier 5%), and the threshold below which no TDS applies rose from ₹15,000 to ₹20,000 of total commission in a financial year. If you haven’t shared your PAN with LIC, the rate jumps to 20%. On Suresh’s ₹14,000 first-year commission, TDS at 2% works out to ₹280, leaving ₹13,720 credited — TDS isn’t your final tax bill, just an advance credit you claim against whatever you actually owe at filing time. From April 1, 2026, the same provision is renumbered as Section 393(1), Table Sl. No. 1(i), under the new Income-tax Act, 2025; the rate and threshold are unchanged, only the section number is new.

GST generally isn’t your problem to manage. Insurance agent services to an insurer fall under the reverse charge mechanism per Notification No. 13/2017-Central Tax (Rate), Entry 7 — LIC itself accounts for and pays the GST on your commission to the government. You don’t need GST registration purely because you earn LIC commission, regardless of how high that income climbs.

The misconception worth correcting directly: many agents assume they can simplify their tax return using the presumptive taxation schemes under Section 44AD or Section 44ADA. Both specifically exclude income earned as commission or brokerage — insurance agency falls squarely in that exclusion regardless of your annual turnover. You’ll need to file as regular business income on ITR-3, deducting your actual business expenses (travel, phone, stationery) rather than applying a flat presumptive rate. We’ve covered the broader filing mechanics, ITR forms, and deductible expense categories in our complete LIC agent guide — the point worth flagging here is narrower: don’t let anyone tell you 44AD or 44ADA is an option for commission income, because it isn’t.

LIC vs Private Insurers vs POSP: Does the Commission Structure Differ?

Since the 2023 regulatory change, every insurer — LIC, HDFC Life, ICICI Prudential, SBI Life, and the rest — sets its own commission structure within its own EoM-approved policy, not a shared IRDAI table. Two insurers can legitimately pay different first-year percentages on a broadly comparable product, and there’s no single “industry standard” rate to benchmark against anymore.

LIC’s scale and brand recognition often offset a marginally lower headline percentage on paper, because persistency — and therefore your renewal-layer income — tends to run higher when the customer recognizes and trusts the insurer behind the policy. That’s not a guarantee, just a structural tendency worth knowing if you’re weighing LIC against a private-insurer agency code.

Corporate agent and bancassurance commission (banks distributing LIC or other insurers’ policies) is typically negotiated at an institutional level and can differ from the individual-agent schedule entirely. A surprising amount of the commission charts circulating online blend corporate-agent rates with individual-agent rates without saying so, which is part of why two sources can quote different numbers for the “same” plan.

The POSP (Point of Sales Person) route is worth knowing about even if you stay with LIC: it offers lower commission ceilings on simplified, standardized products in exchange for a faster, lower-barrier entry — no 25-hour pre-licensing training requirement for the specific products it covers. It’s a relevant comparison if you’re evaluating insurance as one income stream among several rather than committing exclusively to one company’s agency code.

Making the Commission Structure Work for Your LIC Agency Business

Four things are worth carrying forward from everything above. Fixed product-wise commission caps disappeared in 2023, replaced by each insurer’s own board-approved policy. LIC’s commission is built from three layers — first-year, renewal, and bonus — not one flat number, and the October 2024 revision shifted real weight toward the renewal layer. What actually lands in your account after 2% TDS is closer to the headline figure than older 5%-TDS-era expectations suggest, and GST is genuinely not something you need to manage yourself. And there’s no presumptive-taxation shortcut for commission income, so plan your filing around regular business income from day one.

Your next steps: ask your Development Officer for the current board-approved commission schedule for the specific plans you actually sell, rather than relying on a forwarded chart. Model your expected first-year income using the real premium-paying term band of your typical client, not a generic headline percentage. Track your own book’s renewal persistency — it now drives a larger share of your income than it did two years ago. And revisit this once a year, ideally every April, since LIC’s board can revise the schedule again within its EoM policy without it making headlines the way the October 2024 change eventually did.

Understanding the commission structure for a LIC agent in India isn’t just about knowing a percentage — it’s about knowing which percentage applies to what you’re actually selling, and what happens to that number after tax.

Disclaimer: This article is for educational purposes and reflects publicly reported commission ranges and regulatory changes as of mid-2026. Exact commission percentages for specific LIC plans are set by LIC’s internal board-approved policy and can be revised; confirm current rates with your Development Officer or LIC’s official agent portal before relying on them for income planning. This is not tax, legal, or financial advice — consult a Chartered Accountant for guidance specific to your situation.

Frequently Asked Questions

What is the current LIC agent commission rate in 2026?

For most regular-premium LIC plans, first-year commission runs around 25–28% of the annual premium for longer premium-paying terms, dropping to roughly 7.5% in years two and three, and around 5% from the fourth year onward for the life of the policy. Exact rates vary by plan, premium-paying term band, and whether it’s a single-premium product. Confirm the rate for your specific plan with your Development Officer’s current circular.

Why did LIC reduce first-year commission from 35% to 28%?

In October 2024, LIC revised its commission structure alongside new IRDAI surrender value regulations requiring insurers to pay policyholders a higher guaranteed surrender value earlier in the policy term. That reduced the margin available to fund a large first-year commission, so LIC lowered the first-year share from 35% to 28% while raising renewal commission from 5% to 7.5%, shifting more of the payout toward long-term persistency.

Do LIC agents need GST registration for their commission income?

No, not on account of LIC commission alone. Insurance agent services to an insurer fall under the GST reverse charge mechanism (Notification No. 13/2017-Central Tax Rate, Entry 7), meaning LIC itself accounts for and pays the GST on your commission. You aren’t required to register for GST or charge it purely because you earn insurance commission, regardless of how high that income climbs.

How much TDS is deducted on LIC agent commission?

From April 1, 2025, TDS under Section 194D is 2% for individuals once total commission from one payer crosses ₹20,000 in a financial year, down from the earlier 5% rate and ₹15,000 threshold. From April 1, 2026, this provision is renumbered as Section 393(1) under the new Income-tax Act, 2025, with the rate and threshold unchanged. Without a PAN on file, the rate jumps to 20%.

What is bonus commission, and how is it different from renewal commission?

Bonus commission is an additional amount paid over and above the standard first-year commission on many regular-premium plans, while renewal commission is the separate, smaller percentage paid each year the policyholder continues paying. Bonus commission generally isn’t payable on single-premium policies or specific plan numbers LIC excludes.

Can LIC agents file their tax return under the presumptive taxation scheme (44AD or 44ADA)?

No. Both Section 44AD and Section 44ADA specifically exclude commission and brokerage income, and insurance agency commission falls in that exclusion regardless of turnover. LIC agents report commission as regular business income on ITR-3, deducting actual business expenses, rather than using a flat presumptive rate — this is one of the most common misconceptions among new agents.

Does the premium-paying term I sell affect my commission?

Yes, significantly. For most LIC plans, longer premium-paying term bands (commonly 15 years and above) earn a meaningfully higher first-year commission percentage than the same plan sold with a shorter premium-paying term, even at an identical annual premium. This is why agents are trained to recommend the longest premium-paying term a client is genuinely comfortable with.

Is the LIC commission structure the same for individual agents, corporate agents, and POSP?

No. Individual agents, corporate agents (such as banks under bancassurance tie-ups), and Point of Sales Persons (POSP) each operate under separate commission schedules within LIC’s overall Expense of Management policy. Corporate agent rates are often negotiated institutionally and can differ from the individual-agent schedule, while POSP commissions on simplified products are typically capped lower in exchange for a faster, lower-barrier entry process.