Your SIP made about 10% last year. A dollar investor in the very same Nifty made roughly half that. The gap didn’t appear on a single statement – and it is one of the most important numbers in Indian personal finance right now.

Here is a fact that should unsettle anyone who has built their entire wealth on Indian equities.

In the calendar year 2025, the Nifty 50 rose 10.5% in rupee terms, a perfectly respectable year on the face of it. But measured in US dollars, that same index returned only 5.3%. According to NSE data, the index climbed from 23,645 to 26,130 in rupee terms, while the rupee slid from 85.6 to 89.9 against the dollar over the year. Nearly half of your “return” was quietly eaten by the falling currency.

By early June 2026, the picture had worsened. At the June 9 close, the Nifty sat at 23,242, down roughly 7.6% over twelve months and about 12% below its January peak of 26,373. The rupee was near a record low of about 95.2, even after the RBI stepped in with forex-swap facilities to attract dollar inflows; Brent crude hovered around $92.

That divergence of respectable-looking domestic returns and feeble dollar returns is not a footnote. It is the whole story. And it raises a question most Indian investors have never seriously asked: should some of my money be invested outside India?

This article makes the case that the answer is yes but not as a bet against India, but as a correction of a blind spot so large it is, by the numbers, almost impossible to defend. Let us build that case the only way worth building it: with data.

Argument One: The Rupee Is Quietly Taxing You

Start with the currency, because it sits underneath everything else.

Two years ago, a dollar cost about ₹83. By March 2025 it was ₹85.5. Today it is near ₹95.2. In the financial year ending March 2026, the rupee fell 9.88% against the dollar, its steepest annual decline in fourteen years. It briefly touched a record 95.86 in May 2026, making it, at points this year, Asia’s worst-performing major currency.

Why does this matter to you, who earns, spends, and invests in rupees? Because currency depreciation is a hidden tax on your real wealth. When the rupee falls 10%, every imported thing you consume – fuel, electronics, a foreign holiday, your child’s education abroad, costs more. Your nominal portfolio may rise, but its purchasing power against the rest of the world shrinks. That 5-percentage-point gap between the Nifty’s rupee return and its dollar return in 2025 is precisely the size of the tax. You paid for it. You just never saw a receipt.

There is a popular and partly valid rebuttal: the rupee always depreciates, it’s structural, and a long-term domestic investor shouldn’t care. The RBI itself factors depreciation into its projections, and a saver with no foreign liabilities and a 20-year horizon can largely ride it out. Fair enough. But that argument quietly assumes you will never need to convert your wealth into global purchasing power – never travel, never fund an overseas education, never buy anything priced in dollars. For a rising share of India’s affluent class, that assumption is simply false. And the currency is only the first of three forces pulling in the same direction.

Argument Two: The Worst Relative Performance in a Generation

Now layer the equity returns on top of the currency.

In 2025, the Nifty’s 10.5% rupee gain was among its worst relative showings against global peers in decades. The MSCI India index trailed its Asia-Pacific and emerging-market peers by margins not seen since the late 1990s and early 1990s respectively. Those are not ordinary down years. Those are generational gaps.

Consider what other markets did in the same year. South Korea’s KOSPI rose about 76%. Japan’s Nikkei gained 28%. Hong Kong’s Hang Seng rose 29%. China’s CSI 300 climbed 17%. On Wall Street, the S&P 500 added 17% and the tech-heavy Nasdaq 100 advanced 21%. India sat near the bottom of that table.

A single bad year proves nothing as markets are cyclical, and India has compounded handsomely over decades. So extend the horizon. Measured on price charts over the ten years to early 2026, the Nifty 50 returned roughly 107% (7.18% CAGR) in dollar terms. The S&P 500 returned around 255% (10.6% CAGR) over the same window (price returns, excluding dividends). A dollar investor who simply sat in America earned nearly two and a half times what they would have earned in India’s headline index – across a full decade, not a single quarter. The “but India compounds over the long run” argument is true in rupees. In the currency the rest of the world measures wealth in, it has been a decade of meaningful underperformance.

Argument Three: India Doesn’t Sell What the World Is Buying

Here is the structural reason behind the numbers and the most important section of this piece.

Global capital in this decade is chasing a handful of themes: artificial intelligence, semiconductors, advanced robotics, deep tech. Look at what is actually inside the Nifty 50. By weight, it is roughly 20% banks, 11% crude oil, 10% IT services, with the rest spread across autos, finance, telecom, healthcare, FMCG, metals, and infrastructure. Semiconductors do not appear. There is no listed Indian equivalent of a frontier AI company, a chip fabricator, or a robotics pure-play at global scale.

Now look at what an Indian investor confined to the Nifty simply cannot own. Nvidia, the company building the computational backbone of the AI era. TSMC, which manufactures the world’s most advanced chips. ASML, the sole maker of the machines that make those chips. Broadcom, AMD, Micron, Applied Materials, Lam Research, Qualcomm – an entire semiconductor value chain with no domestic counterpart. Add Palantir and CrowdStrike in frontier software, Tesla and Intuitive Surgical in robotics, and a generation of cutting-edge biotech names. None of these can be bought on an Indian exchange.

The contrast is stark when you set the two indices side by side. India’s benchmark is, in essence, a bet on lending money and refining oil. The world’s leading index is a bet on building the future.

This is not a foreigner’s critique. Some of India’s most respected domestic investors say it more bluntly than any outsider would. The veteran investor Ajay Srivastava has likened Indian markets to a frog in slowly warming water, investors who have been “cooked” for two years and stopped noticing, while pointing out that the country’s largest companies pour their growth ambitions into sugar water in the diabetes capital of the world, and asking which global investor would fund that. His prescription is direct: investors need exposure to AI, robotics, quantum computing, and defence, because those themes are not available in India.

Jefferies’ Mahesh Nandurkar has made a related point: the dominant global investment theme remains the AI trade, which is driving money into the US, Korea, and Taiwan, and India doesn’t really feature on that list. When foreign capital rotates toward where the themes are, a market without those themes gets left behind regardless of its domestic strengths.

Sector weight comparison: Nifty 50 vs Nasdaq-100. Nifty is dominated by banks and financials; Nasdaq-100 is dominated by technology and semiconductors.

Approximate sector weights as of mid-2026. Sources: NSE, Nasdaq.

The South Korea Lesson - Why “The Rupee Doesn’t Matter” Misses the Point

The single most instructive counterexample to the “weak currency dooms returns” worry is South Korea and it cuts the opposite way to what you might expect.

Through 2025, the Korean won was weak and foreign investors were net sellers of Korean stocks, dumping roughly 9 trillion won over the year. By the simple logic that weak currency plus foreign selling equals poor returns, the KOSPI should have struggled. Instead it surged about 76% – its best year since 1999 and pushed past 6,000 in early 2026. The reason: a roughly 76% price surge overwhelmed everything else, and South Korea’s long-standing valuation discount began to normalise, its price-to-earnings ratio climbing from about 12.7 to 17.6 over the year.

What drove it? Two things India lacks. First, an AI and semiconductor supercycle, Samsung and SK Hynix, makers of the memory chips feeding the global AI buildout, now account for nearly half of the entire KOSPI’s market capitalisation, and their explosive rally lifted the whole index. Second, the Corporate Value-up Program: a sustained governance reform pushing companies toward higher dividends, buybacks, and better shareholder returns.

The lesson is not “currency depreciation doesn’t matter.” It is subtler and more useful: a weak currency is not what kills foreign returns, weak structural positioning does. Korea had the weak currency and the foreign selling, but it had the themes and the re-rating catalyst, so it ran. India had the weak currency without the themes, so it stalled. The currency was never the deciding variable. The exposure was.

A word of caution belongs here, because honesty is what separates a useful argument from a sales pitch. Korea’s rally is narrow and hot, concentrated in two chip names, fuelled partly by leveraged retail buying, with nearly half the index riding on two stocks. The fund manager Swanand Kelkar’s view is apt: in a rally like this, keep dancing if you must, but dance close to the door. The point of studying Korea is not to chase it. It is to understand why it worked, and what India’s index is missing.

You Are Paying a Premium for Underperformance

One more number completes the picture. Despite the weak performance, Indian equities are not cheap. As of mid-2026, the Indian market’s forward price-to-earnings ratio stood around 20, against roughly 13 for the MSCI Emerging Markets index. India continues to trade at a premium of roughly 50–65% to its emerging-market peers. India has carried this premium for years, even as its multiples stayed flat while markets like Korea and China re-rated upward.

Put the three facts together and the proposition is uncomfortable: you are paying a premium price, for the worst major-market dollar returns in a generation, in a market that offers none of the themes global capital is chasing. Premium price, discount product.

The Number That Should End the Debate

If you take one figure from this article, take this one.

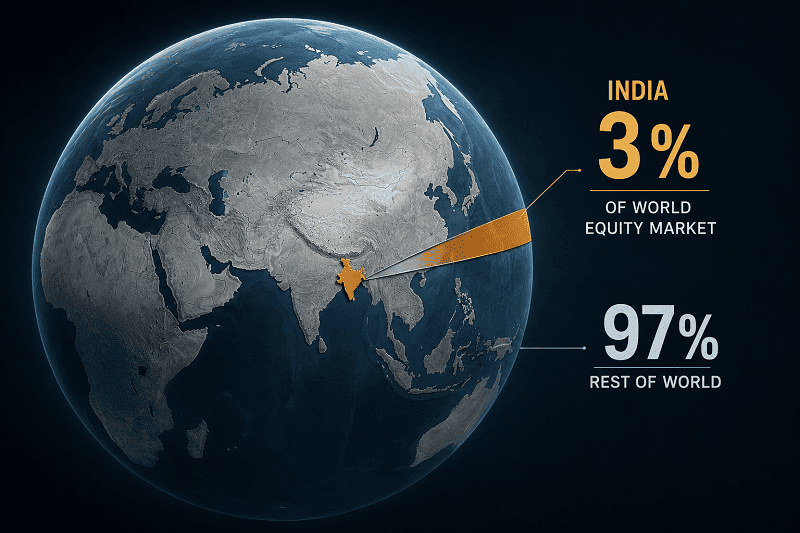

According to an Indian study, Indian investors have kept over 99% of their equity wealth in domestic assets for decades – international allocations are, in their words, “a rounding error away from zero.” Yet India represents only about 3-4% of global market capitalisation.

Sit with that. Indians hold more than 99% of their equity wealth in roughly 3% of the world’s market. That is not conviction but a blind spot the size of the planet. As PPFAS’s Neil Parikh frames it, India is about 4% of world market cap, which means roughly 96% of global opportunity sits outside the only market most Indians own. His case for going global rests on four planks: risk reduction first, the sheer size of the opportunity set, deeper research access, and exposure to themes that simply don’t exist at home.

This is why the case for global investing does not require you to be bearish on India. The argument is not “sell India and buy America.” It is that holding 99% of your wealth in a single country, any single country that is 3% of the world is an extreme, unhedged, and largely unexamined concentration. Even Kelkar, who advises an India-dedicated fund and says he will never remove Indian equities from his core portfolio, personally holds 20–25% of his equity wealth abroad. That is the entire argument, expressed in one professional’s allocation.

So How Does an Indian Actually Invest Globally?

Conviction is easy. Execution, in India, is genuinely difficult and any honest guide has to say so. Here are the real routes, with their real frictions.

The mutual fund route is mostly bolted shut. SEBI caps the entire Indian mutual fund industry at $7 billion of overseas investment, plus a separate $1 billion for foreign ETFs. To grasp how small that is: $7 billion is roughly ₹60,000 crore which is less than 1% of the industry’s ₹80-lakh-crore asset base. The result, in early 2026, was that only around 28 international mutual funds and 6 international ETFs were open to fresh money; the rest re-open only when existing investors redeem and headroom frees up. Funds blink on and off accordingly – Nippon, Axis, and Kotak all paused fresh subscriptions in some overseas schemes through April-May 2026, while Invesco reopened three international fund-of-funds on May 8. It is a game of musical chairs, and you may find the chair full when you arrive.

That leaves three routes that do not count against the $7 billion cap.

The Liberalised Remittance Scheme (LRS). A resident Indian may remit up to $250,000 per financial year to buy foreign securities directly, through an overseas brokerage account. The catch: remittances above ₹10 lakh in a year attract 20% TCS (Tax Collected at Source), though this can be offset against your annual tax liability. And holding US stocks directly in your own name exposes you to a serious, little-known risk – US estate (inheritance) tax of up to 40% on US-situated assets above just $60,000, levied on the total value, not the gains. A pooled fund structure avoids this; a personal brokerage account does not.

GIFT City. India’s International Financial Services Centre at GIFT City is, in regulatory terms, an offshore jurisdiction with its own regulator (the IFSCA), sitting on Indian soil. For Indians investing outbound, it runs on the same LRS limit, but access has improved dramatically. The old $150,000 minimum for global PMS structures has fallen to around $75,000, and significantly for retail investors, some GIFT City feeder funds now start at $5,000 to $10,000. That $10,000 figure is deliberately chosen: it sits just under the ₹10 lakh threshold where 20% TCS kicks in, so a retail investor staying below that ceiling can sidestep the upfront TCS drag entirely.

The tax mechanics within GIFT City matter and they are not all favourable. A GIFT fund investing directly in foreign stocks is taxed on churn,every sale, plus 25% dividend withholding, which is inefficient. So the smarter structures feed into an Irish UCITS fund, where there is no churn tax and dividend withholding is 15%, allowing better compounding. In most of these fund structures the fund pays the tax rather than you, sparing you tax filings in India or GIFT City but redeem within two years and you can be taxed at the 43% marginal rate even in the lowest bracket. Equity held beyond two years is taxed at the 12.5% long-term rate. These are five-to-seven-year products; treat them as such.

India-listed routes. Where headroom exists, India-listed global feeder funds and MNC-themed funds offer indirect exposure without you having to remit anything abroad, though availability is constrained by the same SEBI caps.

What This Actually Means for You

The case for global investing is not a prediction that India will do badly. India remains a rare combination of size and growth, a roughly $4 trillion economy that, growing at around 10% nominally, creates some $400 billion of new GDP every year. Over a 15-to-20-year horizon, in rupee terms, it has compounded at about 12%. A disciplined investor with a long horizon and no foreign-currency needs can reasonably hold a heavy India weighting.

But “reasonable to hold a lot of India” is a world away from “reasonable to hold 99% India.” The three forces this article laid out: a depreciating rupee taxing real returns, a generational stretch of dollar underperformance, and a domestic index structurally missing the themes global capital is chasing, all point in the same direction. They make the case not for abandoning India, but for the simple, overdue act of owning some of the other 97% of the world.

The mechanics are improving and the minimums are falling. The information, now, is in front of you. The hidden currency tax, the missing themes, the 99% concentration, none of these will appear on your portfolio statement. That is exactly why they are worth confronting before the next decade does it for you.

Frequently Asked Questions

Why did a Nifty investor “make nothing” in dollars in 2025 when the index rose 10.5%?

Because the rupee fell about 5% against the dollar over the year (USD-INR moved from 85.6 to 89.9). A rupee return of 10.5% therefore translated to just 5.3% in dollar terms, per NSE data. For anyone whose future spending is partly in foreign currency-overseas education, travel, imported goods, that currency drag is a real loss of purchasing power, even though the rupee statement looked healthy.

Isn’t investing abroad unpatriotic, or a bet against India?

No. The case for diversification is about concentration risk, not loyalty. India is roughly 3-4% of global market capitalisation, yet Indian investors hold over 99% of their equity wealth domestically. Even fund managers who run India-dedicated strategies and remain bullish on India personally hold 20-25% abroad. Owning some of the rest of the world is risk management, not a verdict on India.

What’s the simplest way to start investing globally now that most international mutual funds are closed?

With the SEBI $7 billion industry cap largely exhausted, the open routes are: the Liberalised Remittance Scheme (up to $250,000 a year via an overseas broker), and GIFT City feeder funds, some of which now start at $5,000–$10,000. Staying under ₹10 lakh of remittance in a year avoids the 20% TCS. A handful of domestic international funds and ETFs also reopen periodically when headroom frees up.

What is the 20% TCS on foreign investment, and how do I avoid it?

Remittances abroad above ₹10 lakh in a financial year attract 20% Tax Collected at Source. It is not a final tax. It can be offset against your overall annual tax liability but it locks up cash until then. Investing through a GIFT City route and keeping annual remittance below ₹10 lakh sidesteps the upfront deduction.

Why is South Korea relevant to an Indian investor?

Because it disproves the comforting idea that a weak currency makes foreign returns pointless. Korea’s won was weak and foreigners were net sellers in 2025, yet the KOSPI rose about 76%, its best year since 1999, driven by an AI/semiconductor supercycle and corporate-governance reform. The lesson: structural exposure to the right themes matters far more than currency moves. India had the weak currency without the themes; Korea had both, and ran.

Should I sell my Indian equities and move the money abroad?

The argument here is for adding global exposure, not exiting India. India still compounds at roughly 12% in rupees over long horizons, and a disciplined long-term investor can keep a heavy India weighting. The point is that 99% in a single country, any country that is 3% of the world is an extreme concentration worth correcting, typically by allocating a sensible slice (many advisors suggest 15–25%) to global assets.